The Indian government supports and endorses many savings schemes and investment plans to encourage a culture of savings, ensuring that citizens have a safety net for unforeseen expenses, emergencies, or retirement.

One such scheme is the Kisan Vikas Patra (KVP), introduced by the India Post to encourage small savings and provide individuals with a reliable investment avenue.

What is Kisan Vikas Patra (KVP) Scheme?

The Kisan Vikas Patra (KVP) scheme was introduced by the India Post in 1988 as a savings certificate program. Its primary goal is to encourage small savings and provide investors with a secure future. However, in 2014, the government relaunched the KVP scheme with certain amendments. These amendments required individuals to submit their PAN card proof for investments above Rs. 50,000 and income proof for investments above Rs. 10 lakh. This was done to prevent potential money laundering activities.

KVP certificates can be obtained at any post office across the country. Any individual above the age of 18 years residing in India is eligible to invest in the KVP scheme, and they can choose to get the certificate either in their name or jointly with a minor.

Benefits of Kisan Vikas Patra (KVP)

- KVP guarantees a fixed sum at maturity, regardless of how the market is doing.

- There is no maximum limit on the amount you can invest in KVP.

- You can easily open a KVP account at any post office for your convenience.

- KVP certificates can be used as collateral for secured loans.

- KVP is a risk-free investment option that is not affected by market fluctuations.

- You can start a KVP account with a minimum investment of ₹1,000 and add multiples of ₹100 thereafter.

- The maturity period for KVP is 115 months, during which your investment continues to earn interest.

- You can nominate a beneficiary for your KVP account, ensuring a smooth transfer of benefits.

Pay Anytime, Anywhere!

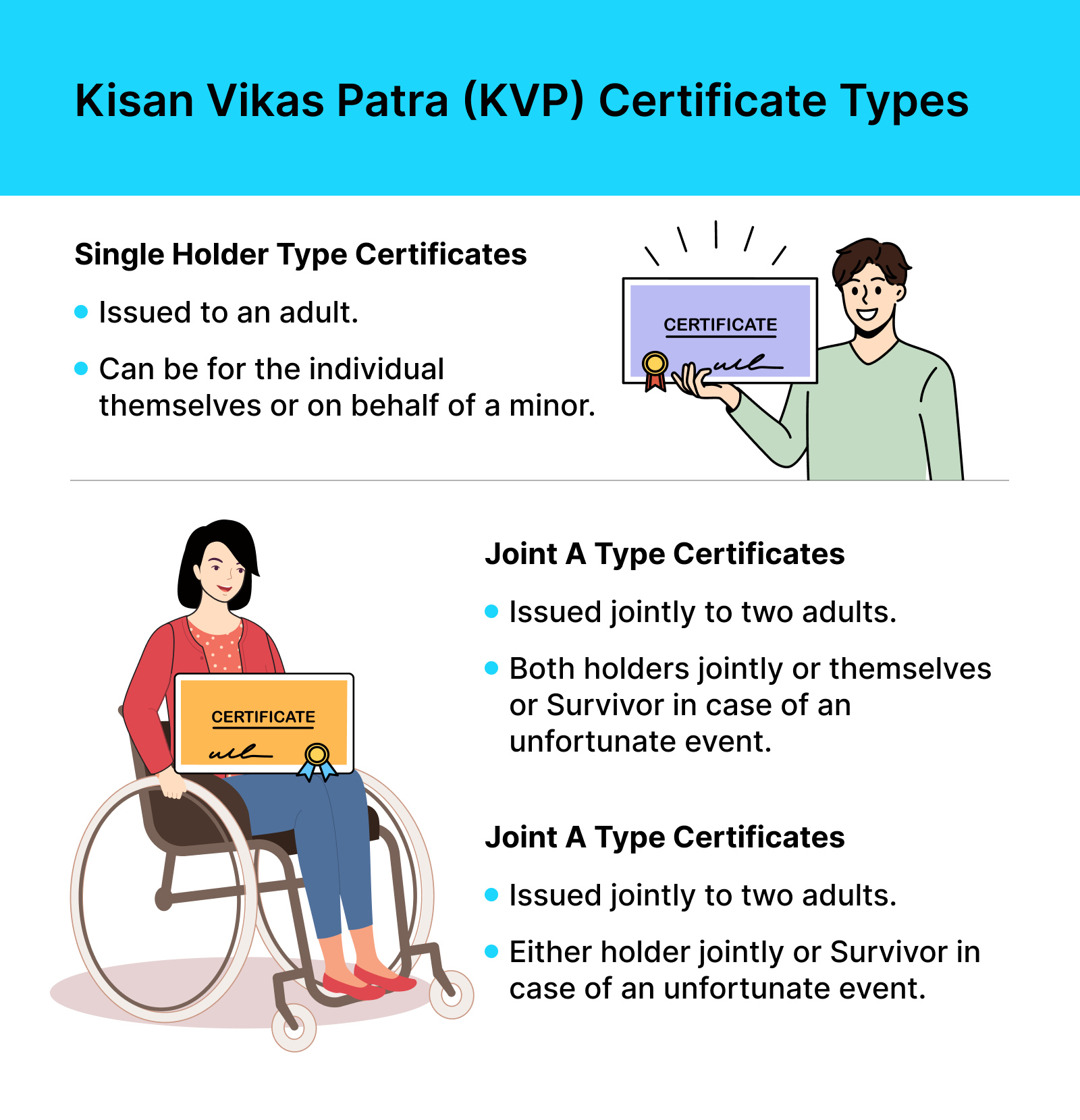

3 Types of Kisan Vikas Patra Certificates

There are three types of certificates available under the Kisan Vikas Patra (KVP) scheme:

- Single Holder Type Certificates: These certificates are issued to an adult, either for themselves, on behalf of a minor.

- Joint ‘A’ Type Certificates: These certificates are issued jointly to two adults. The payment can be made to both holders jointly or to the survivor in case of any unfortunate event.

- Joint ‘B’ Type Certificates: These certificates are also issued jointly to two adults. However, the payment can be made to either holder jointly or to the survivor.

Who Can Invest in Kisan Vikas Patra?

To be eligible to invest in the Kisan Vikas Patra (KVP) scheme, the following criteria must be met:

- The applicant must be an adult and a resident of India.

- In the case of a minor or a person of unsound mind, a parent or guardian may invest on their behalf.

- However, Hindu Undivided Families (HUFs) and Non-Resident Indians (NRIs) are not eligible to invest in the Kisan Vikas Patra scheme.

How to Invest in Kisan Vikas Patra?

Step 1: Log in to your DOP internet banking account.

Step 2: Navigate to ‘General Services’ and select ‘Service Requests‘ followed by ‘New Requests‘.

Step 3: Look for the option ‘NSC Account – Open NSC account and KVP Account‘ to open a KVP account.

Step 4: Enter the desired amount you wish to invest in the NSC account. Note that the minimum amount is Rs 1000, and it should be in multiples of 100.

Step 5: Choose the linked Post Office (PO) savings account as the debit account for the investment.

Step 6: Carefully read and accept the terms and conditions by clicking on ‘Click Here’.

Step 7: Submit the application online.

Step 8: Enter your transaction password to authenticate the transaction and submit the request.

Prerequisites for availing DOP Internet Banking:

- You must have a valid and active Single or Joint “B” Savings account.

- Ensure you have provided the necessary KYC (Know Your Customer) documents.

- An active DOP ATM/Debit card is required.

- You need to have a valid mobile number.

- An email address is necessary.

- You should have a PAN (Permanent Account Number) number.

Activating DOP Internet Banking:

- Visit your home branch and fill out the pre-printed application form.

- Submit the form along with the required documents.

- Your DOP Internet Banking will be activated starting from the next working day.

DOP Internet Banking Activation Confirmation:

Once your request is successfully processed, you will receive an SMS alert on your registered mobile number.

Customer ID:

Your customer ID can be found on the first page of your Passbook. It is the CIF (Customer Information File) ID.

Next Steps After DOP Internet Banking Activation:

- Open the DOP Internet banking page using the URL provided in the activation SMS.

- Click on the “New User Activation” hyperlink.

- Fill in the necessary details and configure your Internet Banking.

Changing User ID:

You can change your user ID once by going to “My profile” and selecting “Update channel login ID”.

Fund Transfer and Deposits:

- You can transfer funds from one POSB account to another, including self-payee or third-party payee.

- Deposits can be made from your SB (Savings Bank) account to your own RD (Recurring Deposit) account, repayment of RD withdrawal, PPF (Public Provident Fund) account, and loan on PPF.

One App for All Payments!

Is Premature Withdrawal Allowed From Kisan Vikas Patra Scheme?

The Kisan Vikas Patra (KVP) has a lock-in period of 30 months, or 2 years and 6 months. You cannot withdraw early from the scheme, except in the event of the account holder’s death or a court order. The account matures after 115 months.

Is KVP Maturity Tax-Free?

Kisan Vikas Patra (KVP) is taxable upon maturity. There are no tax benefits associated with this scheme. The interest earned on KVP is taxable and falls under the category of ‘income from other sources’. It is paid out annually.

In conclusion, any adult resident of India can invest in the Kisan Vikas Patra (KVP) scheme. The scheme offers three types of certificates, and investments can be made individually or on behalf of a minor. However, HUFs and NRIs are not eligible. To invest in KVP, individuals can open an account through DOP internet banking. This requires a valid savings account, completed KYC, and an active DOP ATM/Debit card. Once activated, individuals can perform transactions such as fund transfers and deposits. KVP offers a secure way to save for the future.

Disclaimer: Nothing on this blog constitutes investment advice, performance data or any recommendation that any security, portfolio of securities, investment product, transaction or investment strategy is suitable for any specific person. You should not use this blog to make financial decisions. We highly recommend you seek professional advice from someone who is authorised to provide investment advice.