Kisan Vikas Patra Yojana is a savings certificate scheme, which was launched in the year 1988 by India Post. This is a government-initiated scheme that aims to boost small savings among investors for a secured future. Kisan Vikas Patra, allows investors to invest for the long-term. The maximum tenure of the scheme is of 9 years & 10 months. Initially, KVP was launched specifically for farmers to encourage them to save for the long-term, but now it can be availed by all.

What is Kisan Vikas Patra?

India Post launched the Kisan Vikas Patra, a small-savings certificate programme, in 1988. Its primary goal is to encourage people to practise long-term financial discipline. According to the most recent update, the scheme’s duration is now 124 months (10 years & 4 months).

The minimum investment is Rs. 1000, with no upper limit. And if you make a lump sum investment today, you will receive twice as much at the end of the 124th month. Originally, it was intended to assist farmers in saving for the long term. It is now available to all.

Type of KVP Certificates Available

There are three types of KVP Scheme accounts:

Joint A Type of Account: In this type of account, a KVP certification is issued in the names of two adults. Both account holders would receive the pay-out if the account reached maturity. In the event of the death of one account holder, however, only one would be entitled to the same.

Single Holder Type: A KVP certification is assigned to an adult in this type of account. An adult can also obtain a certification on behalf of a minor; in this case, the certification will be issued in their name.

Joint B Type: A KVP certification is provided in this sort of account in the names of two adults. In contrast to Joint A type accounts, the payout would be made to the survivor or to one of the two account holders upon maturity.

Kisan Vikas Patra Interest Rates 2024

KVP deposits made during the first quarter (January-March) of 2024 will earn an annual compounded interest rate of 7.2%, as announced on December 30, 2022. “The Kisan Vikas Patra (KVP) interest rate is revised by the Union Government on a quarterly basis. The next revision of the KVP interest rate is scheduled to occur by the end of March 2024.”

Eligibility Criteria for Kisan Vikas Patra Yojana 2024

The eligibility criteria for Kisan Vikas Patra Yojana 2024 are as follows:

- A candidate must be at least 18 years old and a citizen of India.

- Adults may submit applications on behalf of minor applicants.

Required Documents for Kisan Vikas Patra Yojana 2024

The following are the documents that must be submitted in order to benefit from the Kisan Vikas Patra Yojana 2024:

- Form A must be properly delivered to an India Post Office branch or one of the designated banks.

- Form A1 should be used when submitting an application through an agent.

- Aadhaar Card, PAN Card, Passport, Voter ID, Driving License, and other KYC documents serve as identification documents.

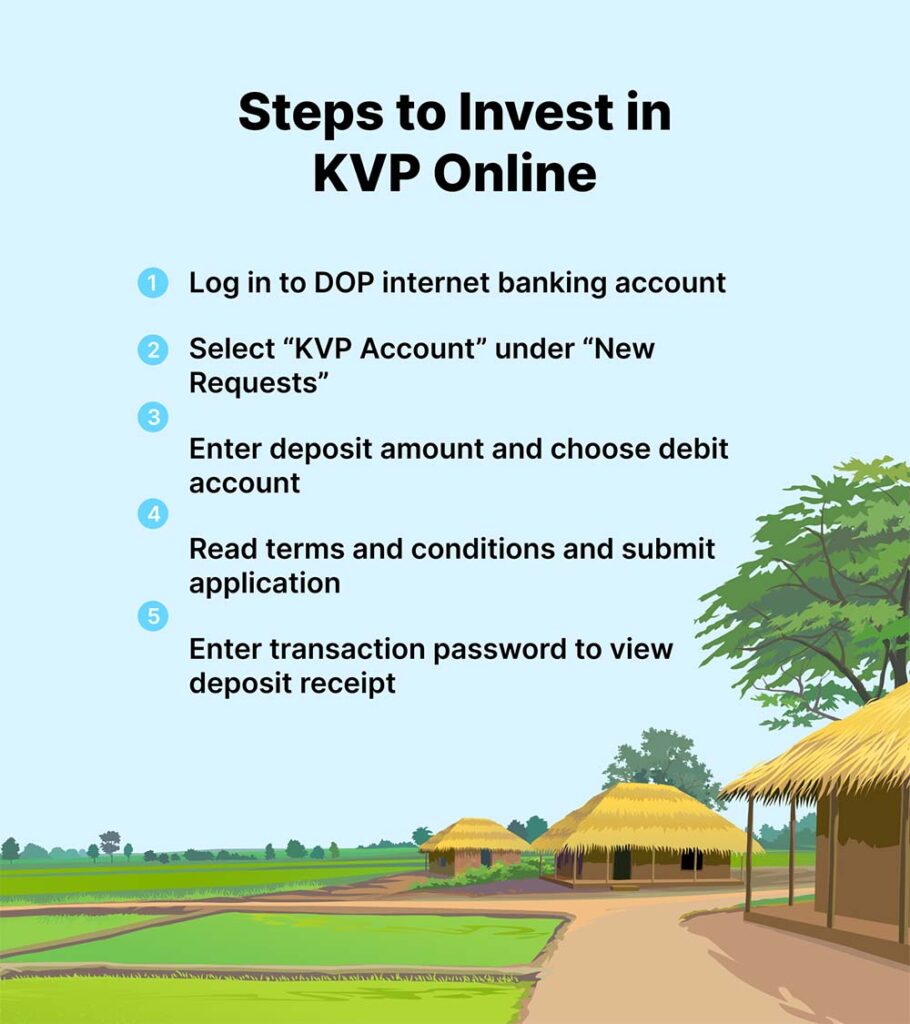

Steps to Invest in Kisan Vikas Patra Online

Follow the given steps to invest in Kisan Vikas Patra online:

- Log in to your DOP internet banking account.

- Select the “New Requests” option after clicking on “Service Requests” under the “General Services” section.

- Choose “KVP Account to open a KVP Account

- Enter the KVP minimum deposit amount and choose your debit account linked to your PO Savings account.

- Click “Click Here” to read the terms and conditions, agree to them, and then submit the application online.

- Enter your transaction password, then click “Submit” to view/download your deposit receipt.

Kisan Vikas Patra Calculator

The maturity amount after a certain period of time from the date of issue can be calculated using one of the many Kisan Vikas Patra Calculators that are easily accessible online. These calculators only require the deposit amount and the investment date. This programme now allows you to earn a 6.9% interest rate. You can currently earn 6.9% interest with this programme.

Tax Benefit on Kisan Vikas Patra

This plan does not provide any tax benefits. The interest is paid on an annual basis and is taxed as “Income from Other Sources.” Furthermore, 10% TDS is deducted from the interest. However, the total amount due at maturity is not tax deductible.

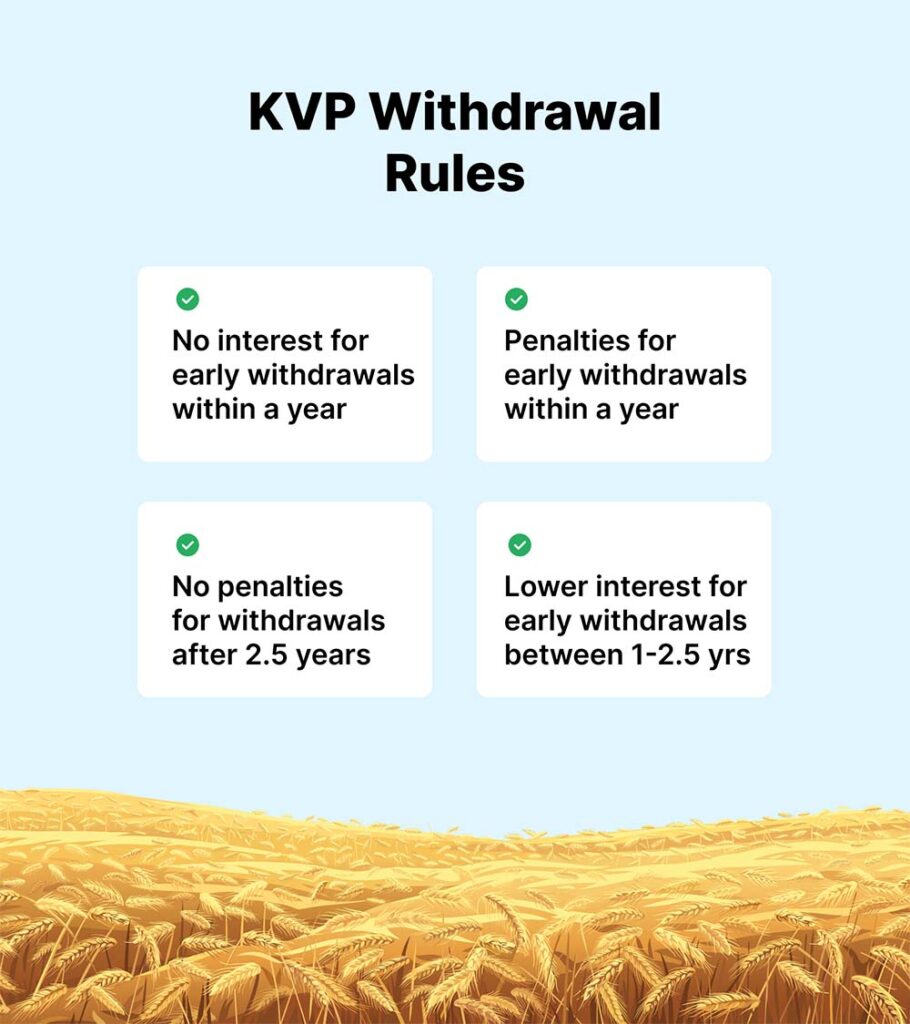

Kisan Vikas Patra Withdrawal Rules

Investors may withdraw their money at any time under the terms of the plan, but there are several restrictions:

- There will be no interest paid on early withdrawals made within a year. In accordance with the rules of the plan, the investor will also be penalised.

- A lower rate of interest will be paid on early withdrawals made after a year and up to 2.5 years.

- Premature withdrawals after 2.5 years are not subject to penalties, but are still subject to the applicable rate of interest.

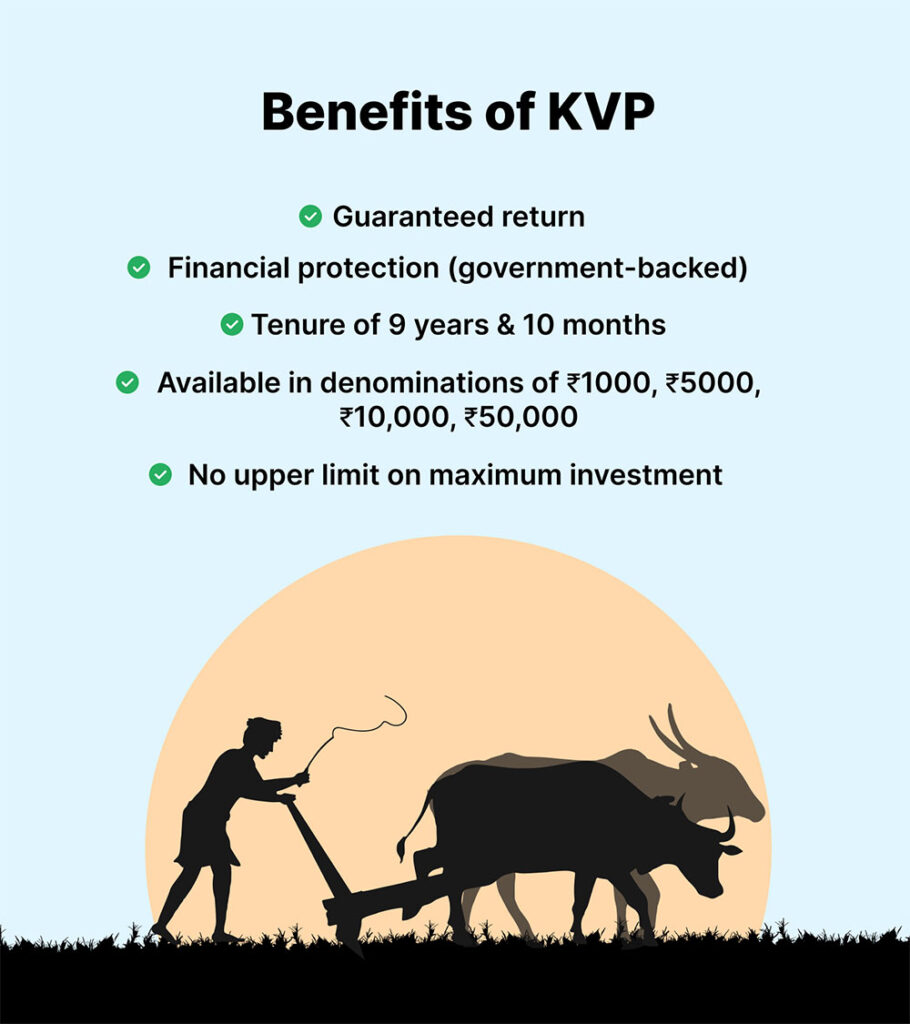

Benefits offered by Kisan Vikas Patra

As a government-backed savings scheme, Kisan Vikas Patra is considered one of the safest options for investment. Along with the benefit of the lucrative interest rate, there are various other benefits offered by KVP. let’s take a look at these benefits:

1. Guaranteed Return

As a government-backed savings scheme, KVP guarantees a profitable return on investment over a long-term period. This means that after completion of the tenure of the scheme, a guaranteed maturity benefit is offered to the account holder as accumulated funds.

2. Financial Protection

As KVP is a government-initiated scheme it is not subject to market risks. The scheme ensures financial security for the long term. The certificates of KVP are available in denominations Rs.1000, Rs.5000, Rs.10,000 and Rs.50,000. However, there is no upper limit on the maximum amount of investment.

3. Tenure

The scheme offers a tenure of 9 years & 10 months (118 Months) to the investors. The principal amount invested in Kisan Vikas Patra is doubled in 112 months i.e. 9 years & 4 months. Once the tenure of the scheme is completed the account holder can withdraw the money. Moreover, the interest will continue to accrue on the accumulated amount, till the time the account holder withdraws the money.

4. Loan Facility Against KVP

An individual can use the Kisan Vikas Patra certificate as security or collateral to avail of a secured loan. However, the interest rate applicable in such a loan is comparatively low.

5. Nomination Facility

KVP offers a very simple and hassle-free facility to nominate a nominee. The subscriber just needs to collect a nomination form from the post office and fill it out thoroughly. If the nominee is a minor, then the account holder will be required to submit the birth certificate and mention the minor’s birth date.

Also Read: Pradhan Mantri Suraksha Bima Yojana & Pradhan Mantri Jeevan Jyoti Bima Yojana

Conclusion

The following considerations should be made when investing in Kisan Vikas Patra:

- The application must be addressed to the relevant Postmaster General of the Post Office being submitted.

- The purchase price must be specified in the form.

- Mention whether the KVP subscription is purchased as a single, joint ‘A,’ or joint ‘B.’ Include the names of both beneficiaries if it is purchased jointly.

- Include the beneficiary’s date of birth (DOB), parent’s name, and guardian’s name if he or she is a minor.

- The nominee’s full name, date of birth, and address must be included on the form (if any).

- Following the submission of the form, a KVP certificate with the beneficiary’s name, maturity date, and amount will be issued.

- Avoid editing and rewriting.

- The KVP form can be purchased with cash or a cheque.

- Include the cheque number on the form if you are paying by cheque.