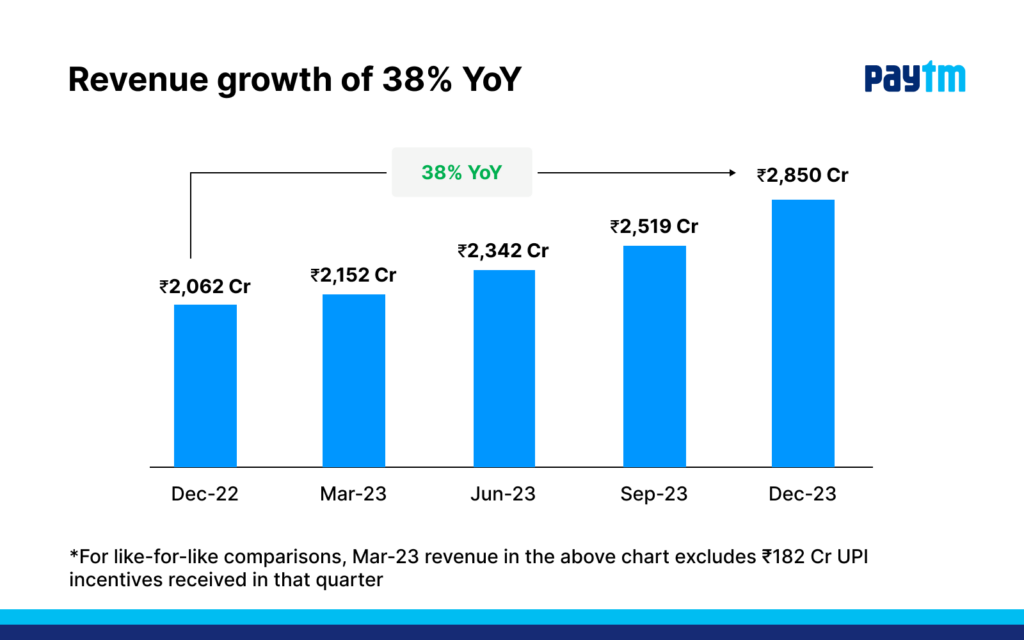

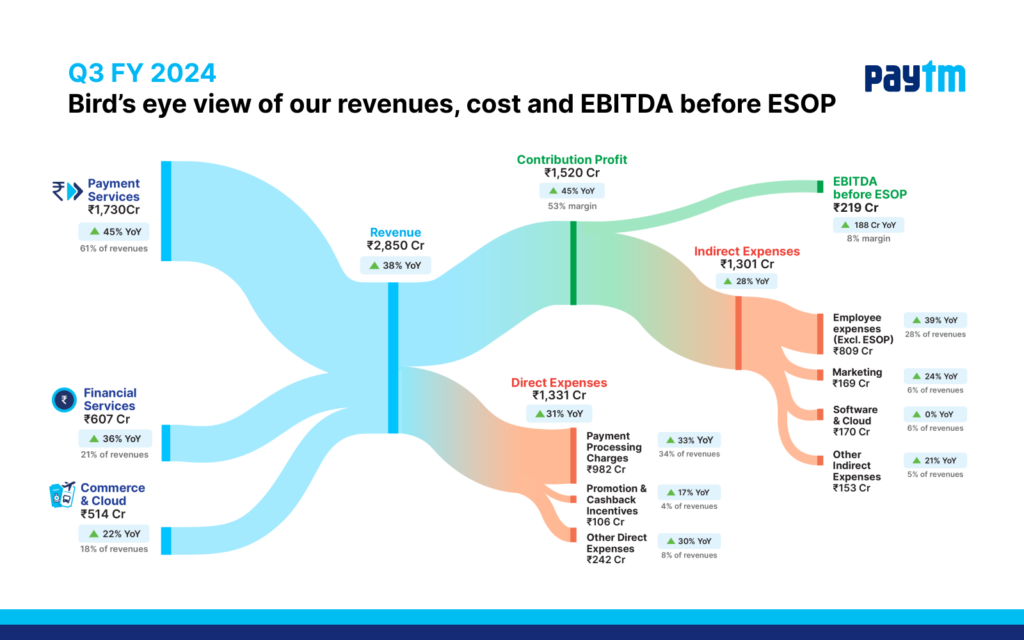

We have announced our Q3FY24 results today. Driven by sustained GMV growth, higher device addition, and expansion of the financial services business, our strong growth momentum continues. Our revenue from operations has seen a growth of 38% YoY to ₹2,850 Cr, and EBITDA before ESOP has increased to ₹219 Cr as compared to ₹153 Cr in Q2FY24 (excluding UPI incentives). Our PAT improved by ₹170 Cr YoY to (₹222 Cr).

Our payments revenue increased 45% YoY to ₹1,730 Cr while the payments profitability improved with net payment margin expanding 63% YoY to ₹748 Cr. Due to the increase in GMV of non-UPI instruments like EMI and cards, and improvements in payment processing margin, our net payment processing is within the 7 to 9 bps range. In Q3FY24, our merchant payments volume (GMV) grew 47% YoY to ₹5.1 Lakh Cr.

Revenue from financial services and others grew 36% YoY to ₹607 Cr in Q3FY24, while the value of loans distributed grew to ₹15,535 Cr, up by 56% YoY. As communicated earlier about our focus on high-ticket loans, we have distributed ₹490 Cr of high-ticket loans in the quarter. We saw a large opportunity in the high-ticket loan business as we have over 2 Cr whitelist loan customers. The total number of unique borrowers who have taken a loan through our platform has increased by 44 Lakh in the last year to 1.25 Cr.

You can read the full Q3FY24 financial results report here: https://www.bseindia.com/xml-data/corpfiling/AttachLive/8409e86f-34dd-42bc-b7db-c7478a10e7a8.pdf

In Payments, our multi-device-led strategy will further strengthen acquiring leadership. We will also focus on new use cases like Credit on UPI, Autopay, etc. to lead monetisable incremental customer acquisition. In Marketing Services, we are offering Deals, Gift vouchers, Loyalty, and enabling commerce services to merchants along with advertising on our App for various brands and businesses. Under financial services, we are expanding high-ticket loans by focusing on adding new lending partners. We are also scaling embedded insurance and merchant insurance offerings and cross-selling equity trading to our consumer base.

We continue to monetise our app traffic in our Marketing Services (erstwhile Cloud and Commerce) segment, which includes deals and gift vouchers, ticketing (travel, movie, events, etc.), advertising, and credit cards marketing, etc. In Q3FY24, our Marketing Services revenue grew by 22% YoY to ₹514 Cr.

Our contribution profit of ₹1,520 Cr represents a growth of 45% YoY driven by an increase in net payments margin and financial services, while the contribution margin improved to 53% from 51% a year ago. Our EBITDA before ESOP improved to ₹219 Cr as compared to ₹153 Cr in Q2FY24 (excluding UPI incentives), while margin stood at 8% on account of consistent improvement in profitability due to strong revenue growth, increasing contribution margin and operating leverage.

Our focus on AI-led efficiency is set to further drive operating leverage. In the current quarter, our indirect expenses (as a % of revenues) have declined to 46%, from 49% in Q3FY23.

User engagement on the platform continues to grow with average Monthly Transacting Users (MTU) of 10 Cr, a jump of 17% YoY. With 47% YoY growth in our App GMV, consumer engagement on our app continues to remain strong. There’s an increasing trend of customers linking our RuPay credit cards to payment apps and using them to make payments on UPI QR code.

Leadership in payment monetisation continues with 1.06 Cr devices, both Soundbox and Paytm Card Machines deployed, increasing 49 Lakh YoY (82% growth YoY) and 14 Lakh QoQ. Our merchant subscriber network has crossed the 1-crore benchmark and grew by 14 Lakh for the quarter.

We remain grateful for your continuous support and remain committed to our mission to building a profitable company and creating shareholder value while driving digitization and inclusive financial access