Filing your income tax return on time is important for a few simple reasons. Firstly, it helps you avoid penalties and late fees from tax authorities. This means you won’t have to pay extra money unnecessarily. Secondly, filing on time ensures that you can claim any tax refunds you’re eligible for without any delays. This means you’ll get your money back as soon as possible.

Filing on time helps you avoid any legal problems like tax audits or investigations. Lastly, timely filing of income tax is often required when you want to apply for loans, mortgages, or visas. It shows that you’re responsible with your finances and can help you access these opportunities easily.

Documents and other Prerequisites for Filing e-Filing ITR

Documents You’ll Need

- PAN card: Your PAN status must be active and it must be linked with your Aadhaar

- Aadhaar card: As per Section 139AA of the Income Tax Act, individuals are required to furnish their Aadhaar card information when submitting their tax returns.

- Form 16: It is a crucial document for filing ITR as it provides a detailed summary of the income earned by you and the taxes deducted at source (TDS) by your employer. Form 16 consists of Part A and Part B. Part A provides details on TDS, including your employer’s PAN and TAN details. Part B provides details on TDS calculations, encompassing the gross salary, exempt allowances, perquisites, and other relevant information.

- Form-16A/ Form-16B/ Form- 16C: Form-16A is issued by deductors like banks etc., for TDS on non-salary payments like FDs, RDs etc. Form-16B is issued for TDS on property sale by the buyer. Form-16C is a TDS certificate for 5% rent deduction under section 194IB. Those deducting TDS on rent provide Form-16C to payees.

- Bank account details: Mandatory disclosure of all active bank accounts is required in the ITR, including bank name, account number, IFSC code etc.

- Bank statement and passbook: Bank statements summarize interest earned on savings accounts and fixed deposits, crucial for filing your ITR.

- Form 26AS and AIS/TIS: Both these documents are crucials while filing ITR. Form 26AS can be accessed through the income tax e-filing portal. Income Tax Department has recently launched “AIS for Taxpayers” app. AIS-TIS is a record that includes information about a taxpayer’s income, financial transactions, tax details, and income-tax proceedings.

- Home loan statement: You can get it from your bank/loan company from where you’ve taken the home loan

- Relevant documents for tax saving instruments like ELSS, FDs etc

- Rental income: If you earn rental income from a property, you must report it

- Documents showing capital gains earned from shares, properties, securities etc

- Dividend income: Report dividend income from shares or mutual funds when filing your income tax return.

- Income overseas: If you’ve earned income from a job deployment overseas, you must furnish the details

Other Prerequisites You’ll Need

- You must be a registered user on the e-filing portal and have a valid user ID and password.

- It is recommended to pre-validate at least one bank account and nominate it for a refund.

- You must have a valid mobile number linked with Aadhaar, e-filing portal, your bank, NSDL, or CDSL for e-verification.

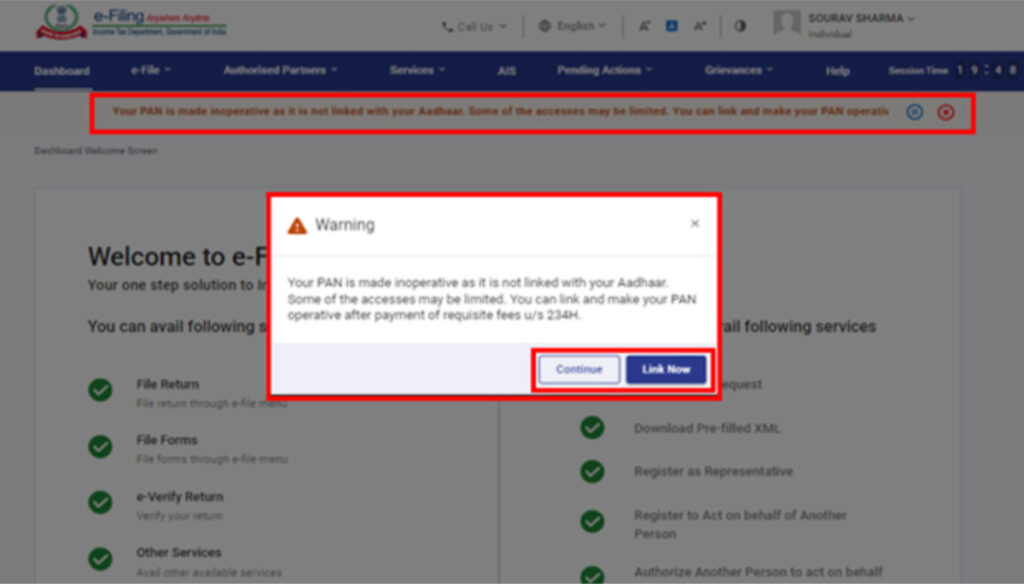

Note: If your PAN is not linked to your Aadhaar, your PAN will become inoperative. In such cases, you will receive a message stating, “Your PAN is made inoperative as it is not linked with Aadhaar. Some accesses may be limited. You can link your PAN and make it operative after payment u/s 234H.

Under Section 234H, there is a Rs 500 penalty for linking PAN to Aadhaar between April 1, 2022, and June 30, 2022. However, if the linking is done on or after July 1, 2022, the penalty increases to Rs 1,000.

Also Read: Types of ITR Forms

How to File ITR Online?

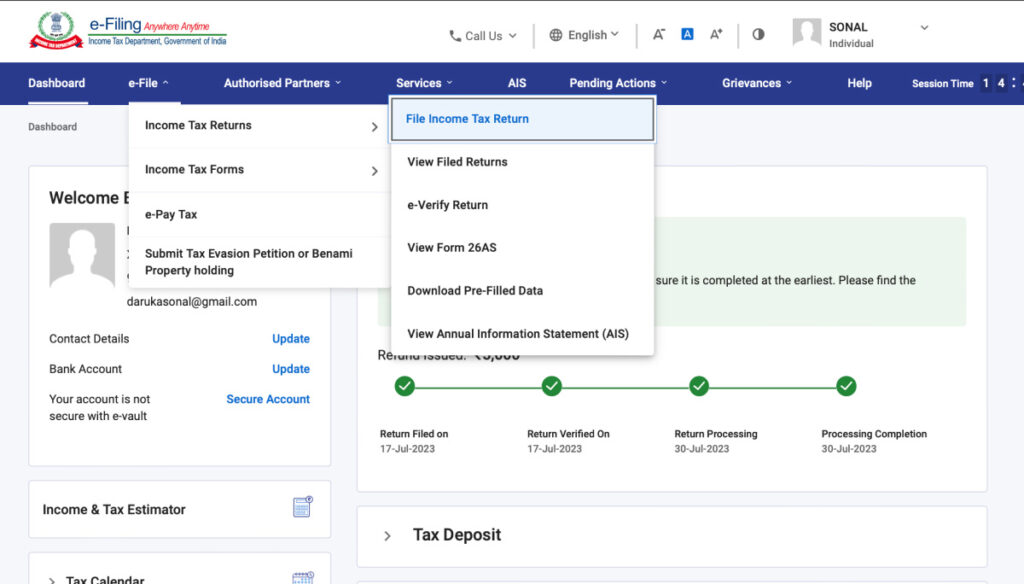

Step 1: Login to the e-filing portal with your user ID and password.

Step 2: Once you’re on your dashboard, navigate to e-File > Income Tax Returns > File Income Tax Return.

Note: If your PAN is considered inoperative because it’s not linked with Aadhaar, you will receive a warning message. You can choose to link your PAN with Aadhaar by clicking on the “Link Now” button, or continue without linking. However, if it’s not been linked already, you’re required to pay INR 1000 as a penalty.

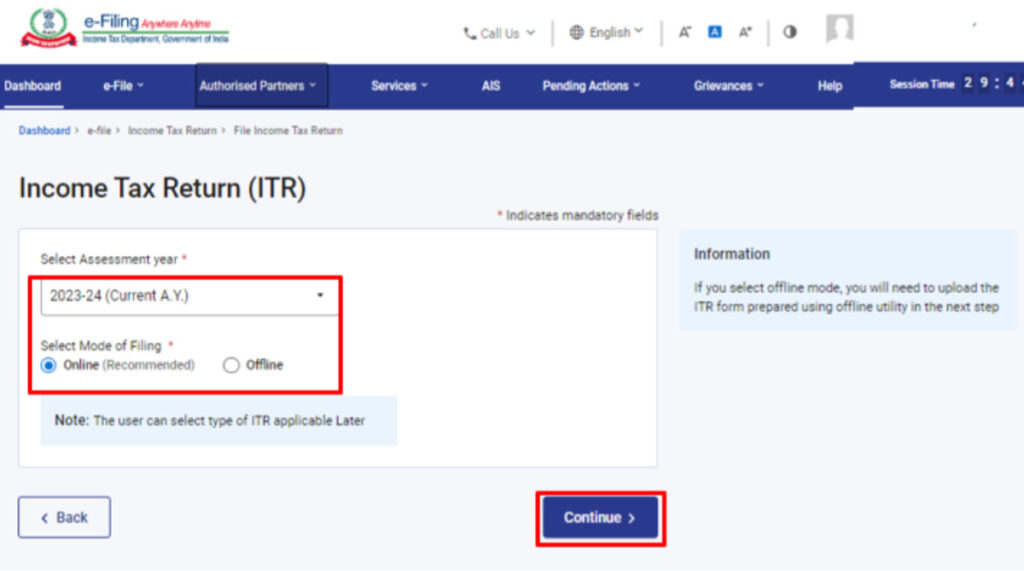

Step 3: Select the assessment year as 2023-24 and choose the online mode of filing. Click on ‘Continue’ to proceed.

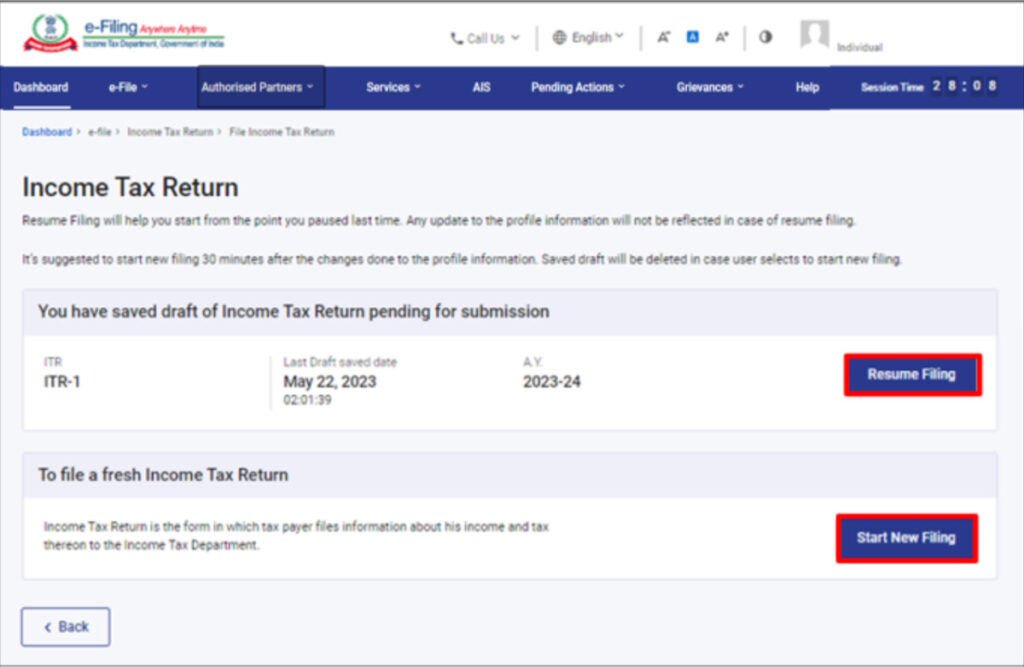

Step 4: If you have already filled the ‘Income Tax Return’ and it is pending for submission, click on “Resume Filing“. If you wish to discard the saved return and start preparing a new one, click on “Start New Filing“.

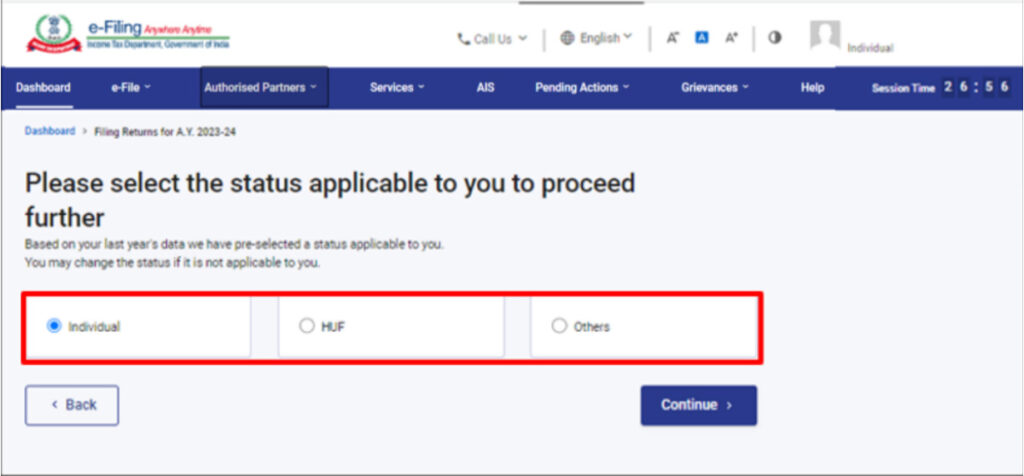

Step 5: Select the appropriate status that applies to you and click on “Continue” to proceed.

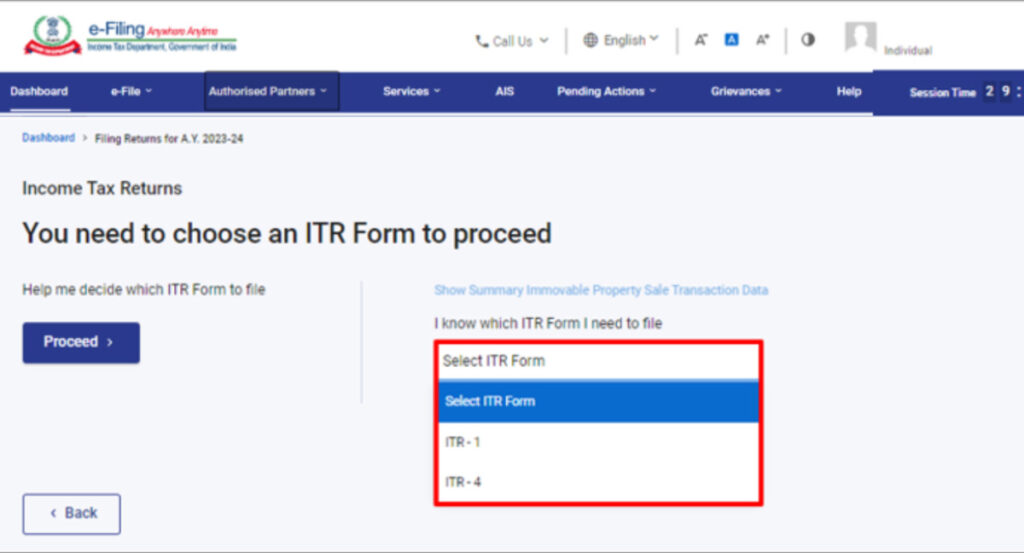

Step 6: You have two options for selecting the type of income tax return:

- If you already know which ITR form to file, select the specific form.

- If you are unsure about which ITR form to file, you can choose “Help me decide which ITR Form to file” and click on “Proceed“. The system will assist you in determining the correct ITR form, and then you can proceed with filing your return.

Note: If you are unsure about the applicable ITR form or schedules, or if you are unsure about your income and deduction details, answering a set of questions will help determine the correct forms and schedules for error-free filing.

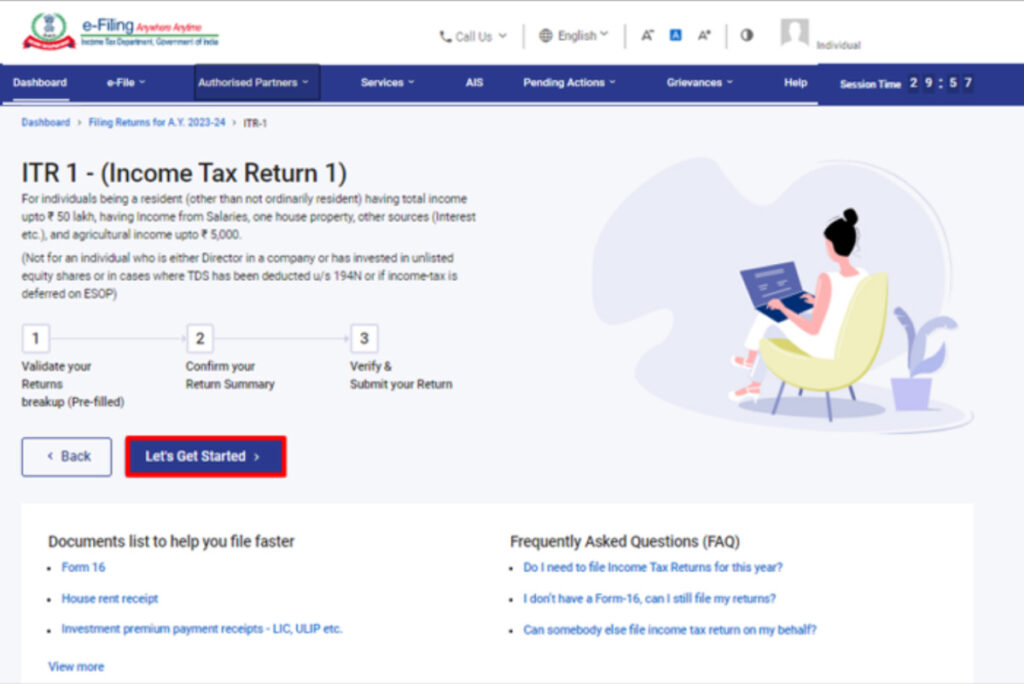

Step 7: After selecting the applicable ITR form, make a note of the required documents and click on “Let’s Get Started“.

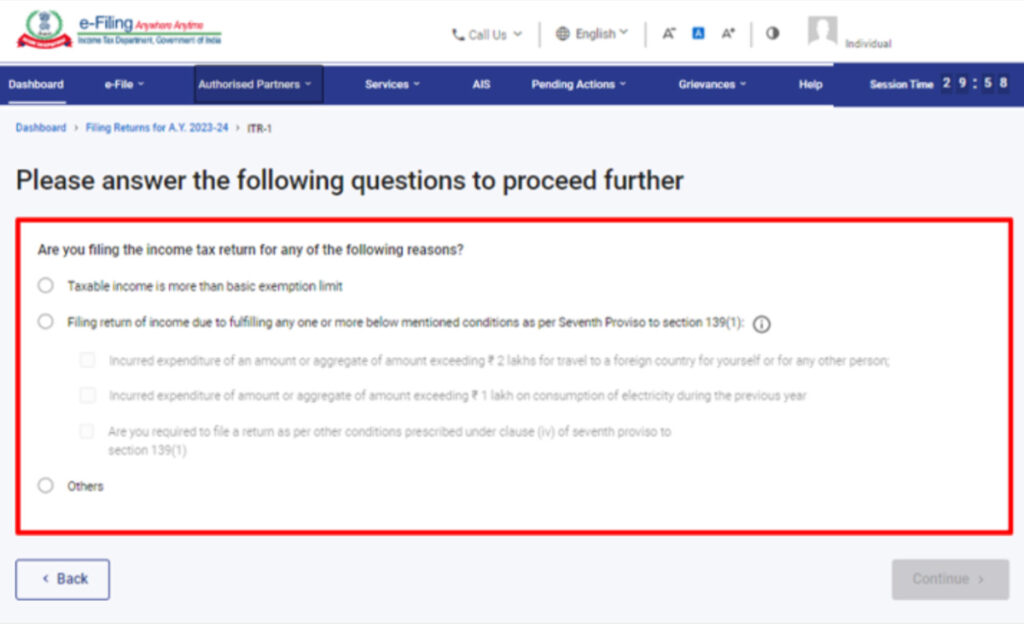

Step 8: Select the checkbox that corresponds to your reason for filing the ITR and click on “Continue“.

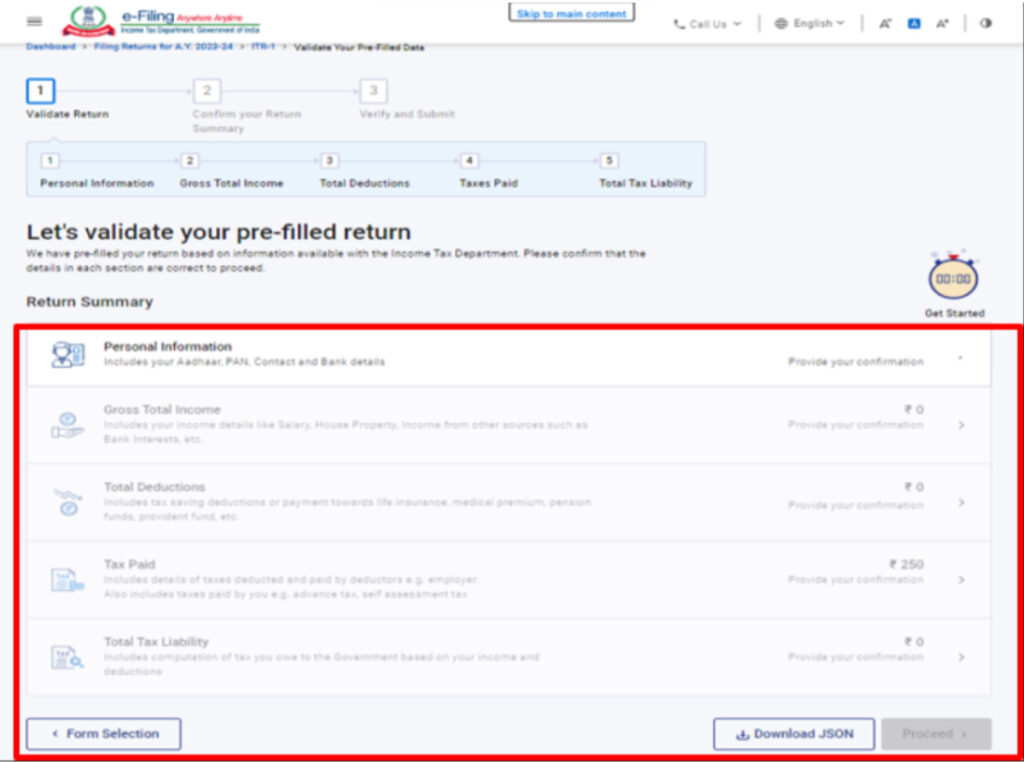

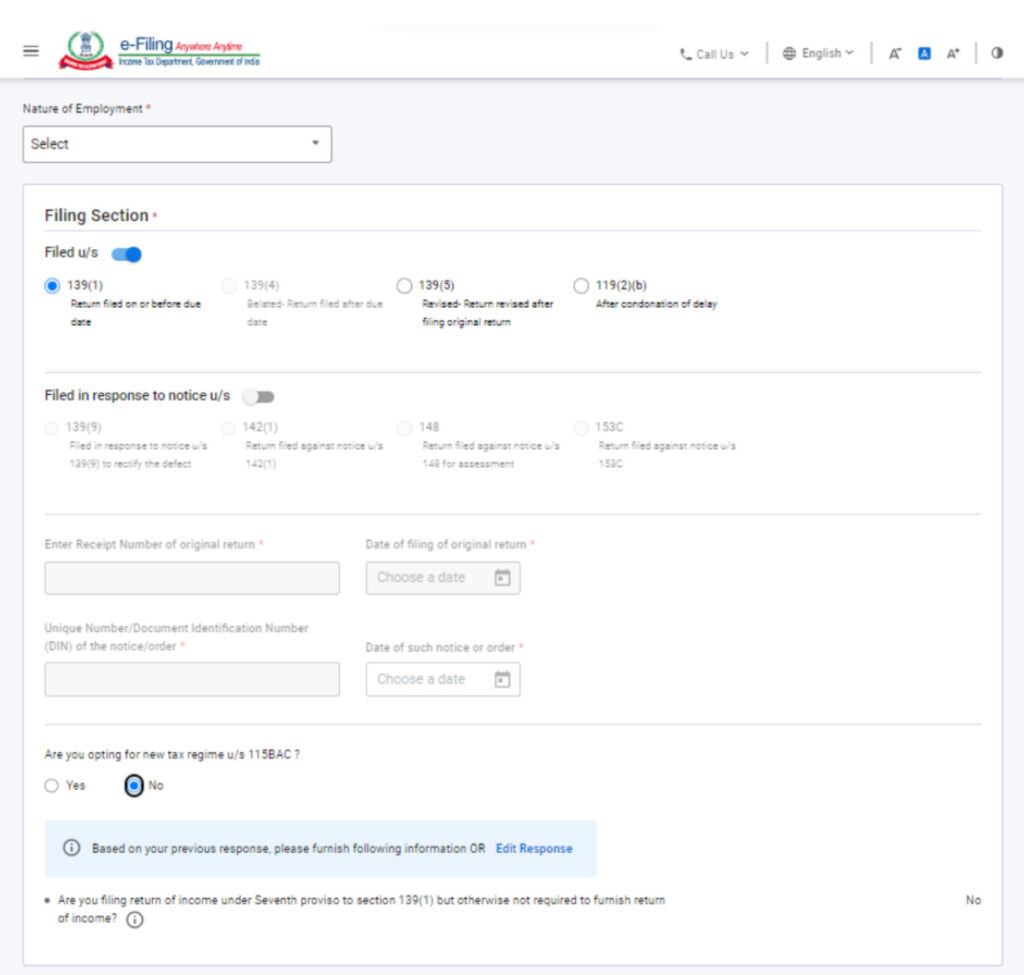

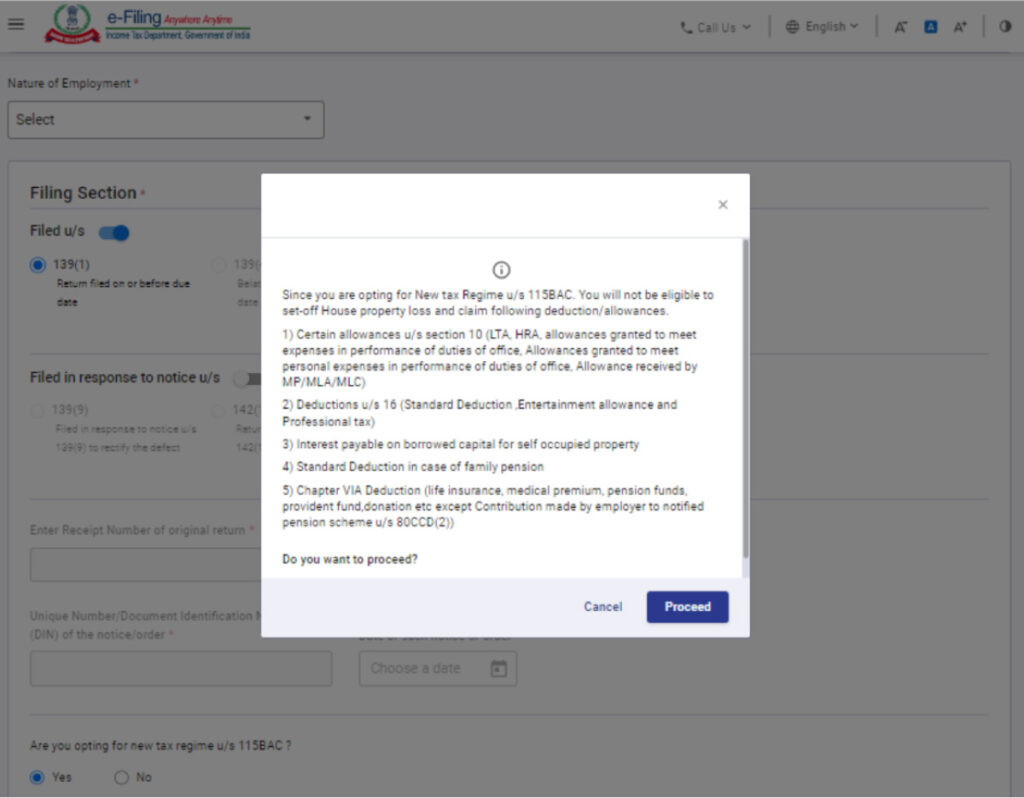

Step 9: If you want to choose the ‘New Tax Regime’, select “Yes“ in the personal information section. Review your pre-filled data and make changes if needed. Enter any additional or remaining data as required. Finally, click on “Confirm” at the end of each section.

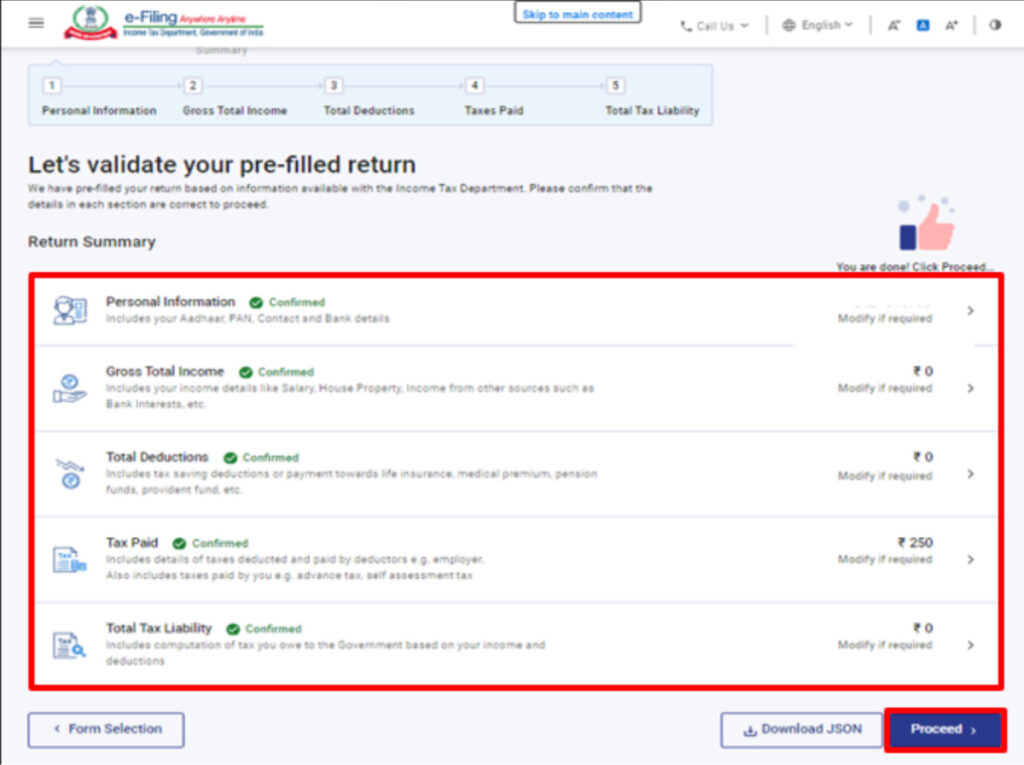

Step 10: Enter or edit your income and total deductions details in the relevant sections. Once you have completed and confirmed all sections of the form, click on “Proceed“.

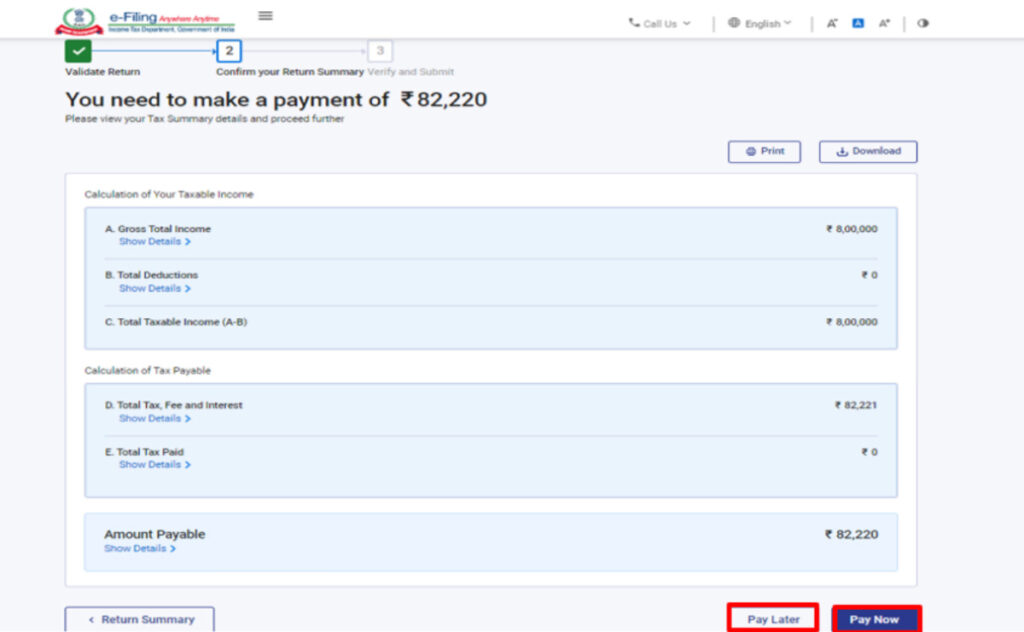

Step 10a: If you have a tax liability, click on “Total Tax Liability” to view a summary of your tax computation based on the details you provided. If there is a tax liability payable according to the computation, you will see the options “Pay Now” and “Pay Later” at the bottom of the page.

Note: It is advisable to use the “Pay Now” option for paying your tax liability. If you choose the “Pay Later” option, you can make the payment after filing your Income Tax Return. However, note that there is a risk of being considered a taxpayer in default, and you may be liable to pay interest on the tax payable.

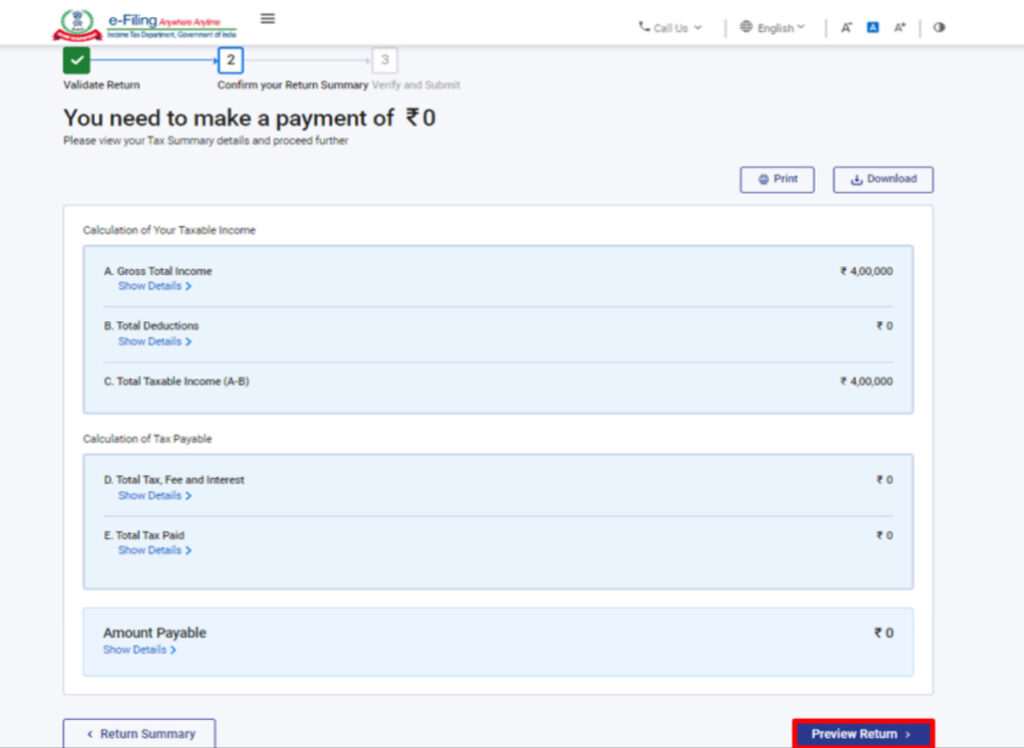

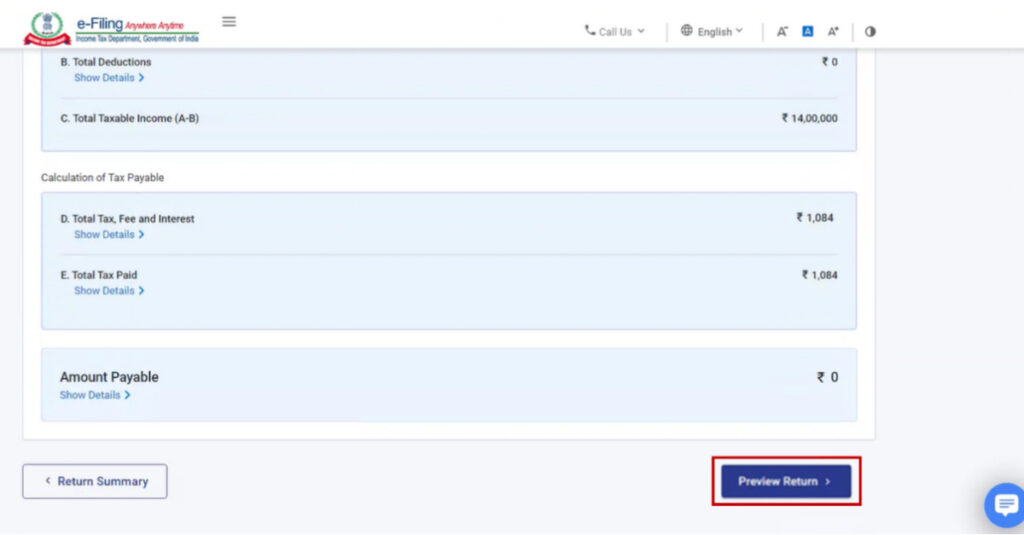

Step 10b: If there is no tax liability (No Demand / No Refund) or if you are eligible for a refund, click on “Preview Return“. If there is no tax liability payable or if there is a refund based on the tax computation, you will be directed to the “Preview and Submit Your Return” page.

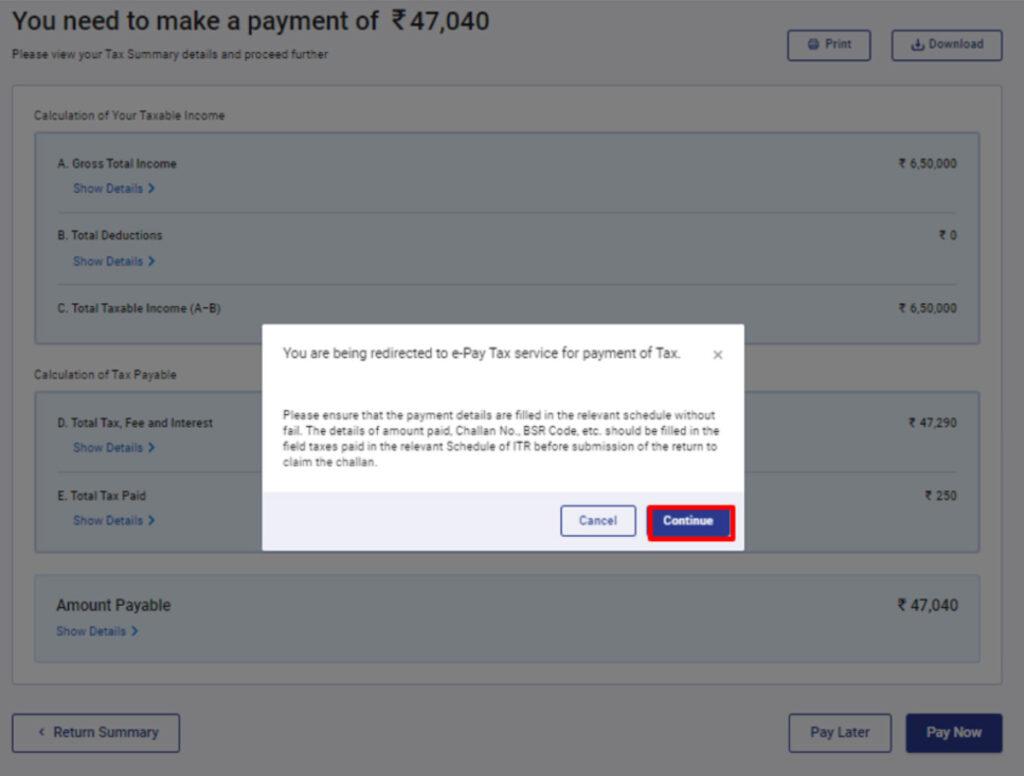

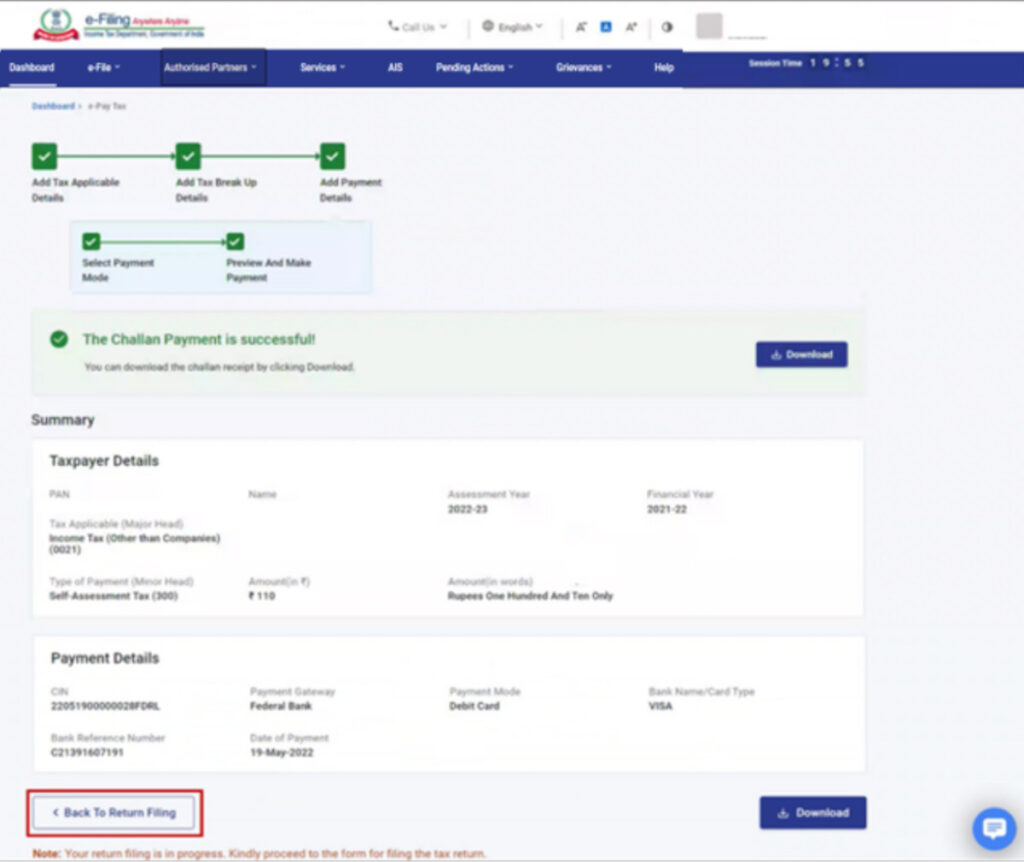

Step 11: If you choose to click on “Pay Now,” you will be redirected to the e-pay Tax service. Click on “Continue” to proceed.

Step 12: After successful payment, click “Back to Return Filing” to complete filing the ITR.

Step 13: Click ‘Preview Return’.

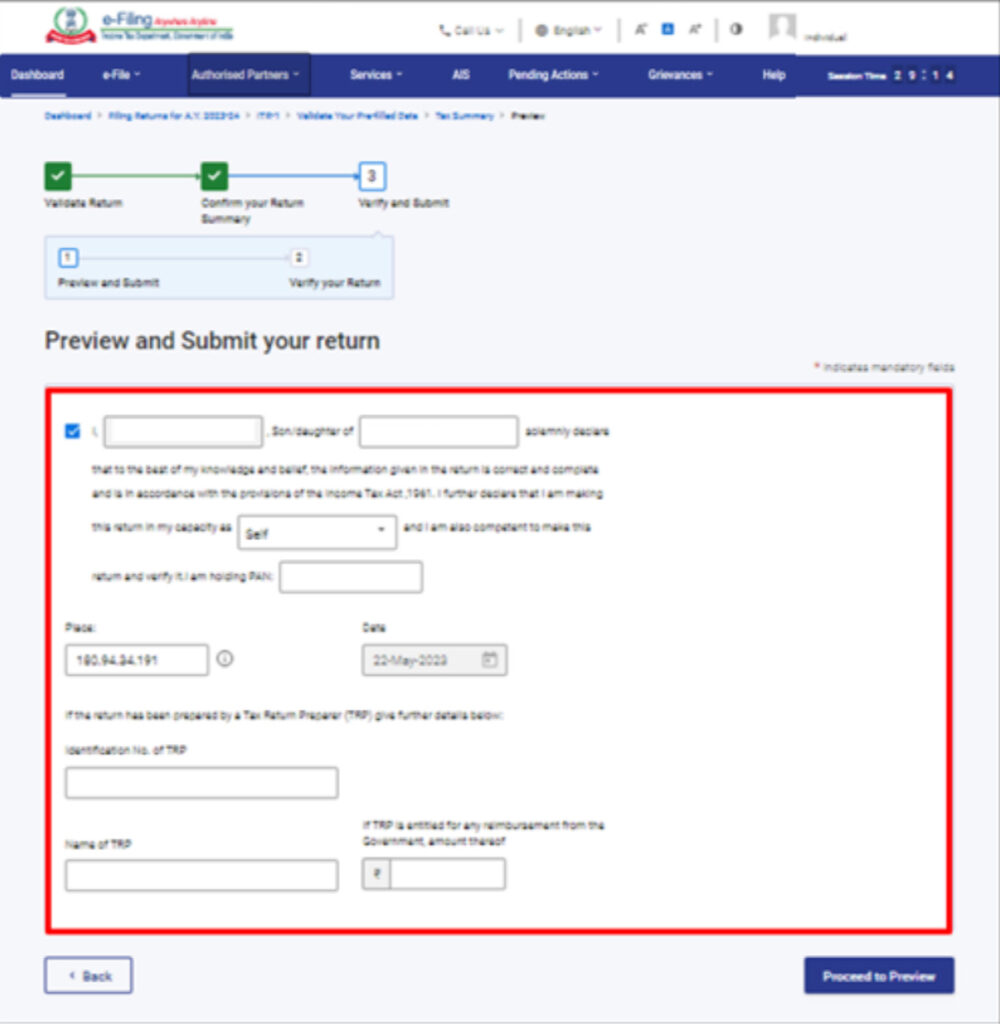

Step 14: On the “Preview and Submit Your Return” page, check the declaration checkbox and proceed to preview

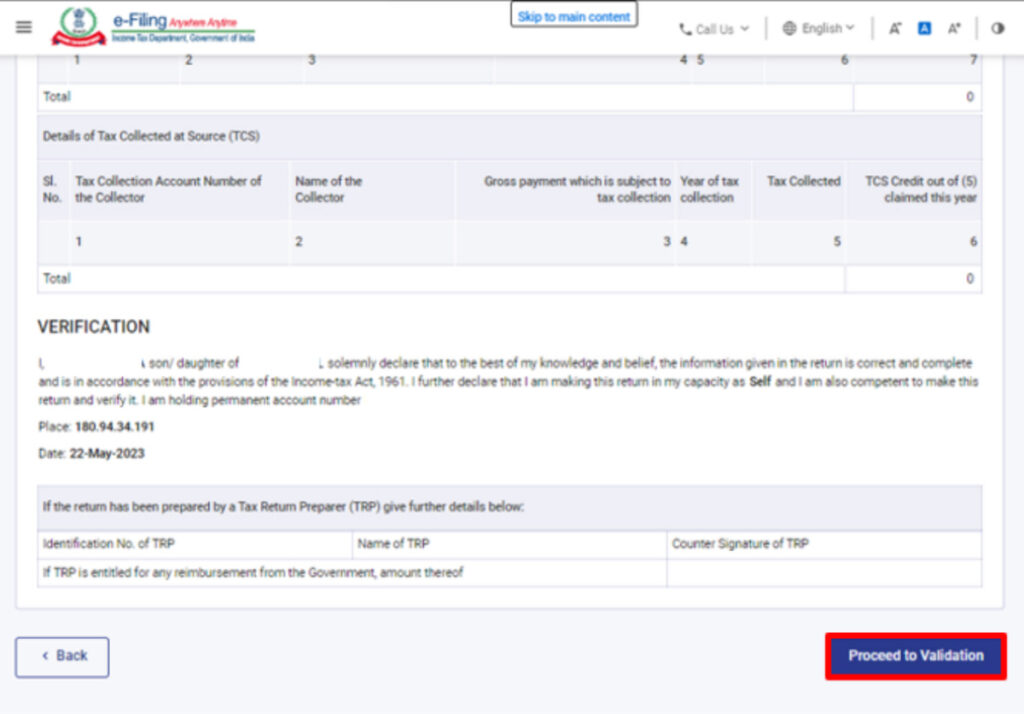

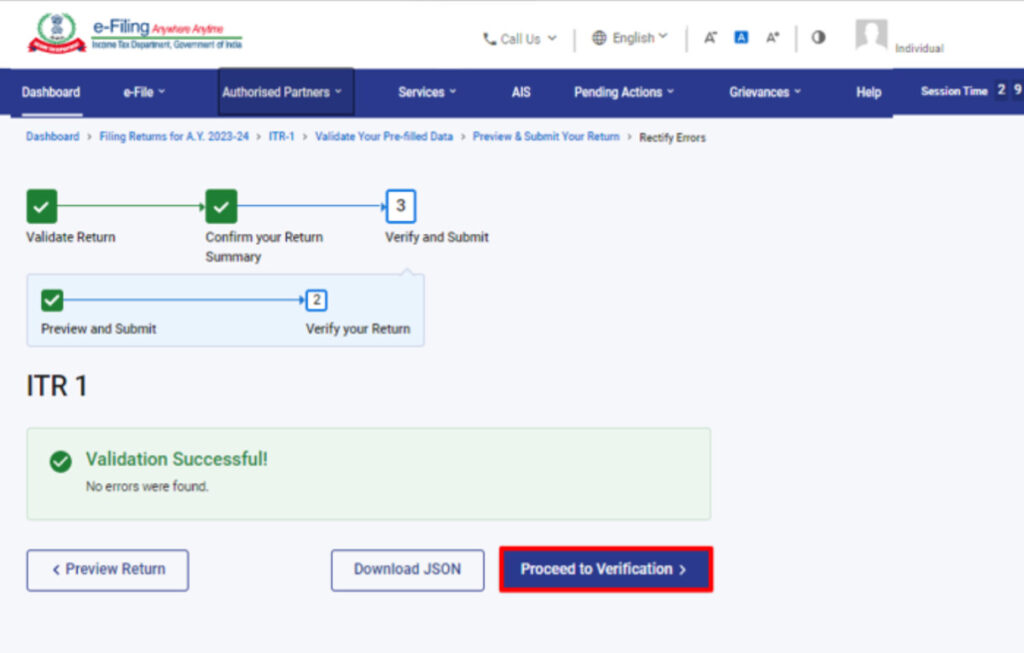

Step 15: Preview your return and proceed to validation by clicking on the “Proceed to Validation” button.

Step 16: Once you have validated your return, click on “Proceed to Verification” on the ‘Preview and Submit Your Return’ page. If you encounter any errors in your return, you must go back to the form to correct them. If there are no errors, you can proceed to verify your return by clicking on “Proceed to Verification.”

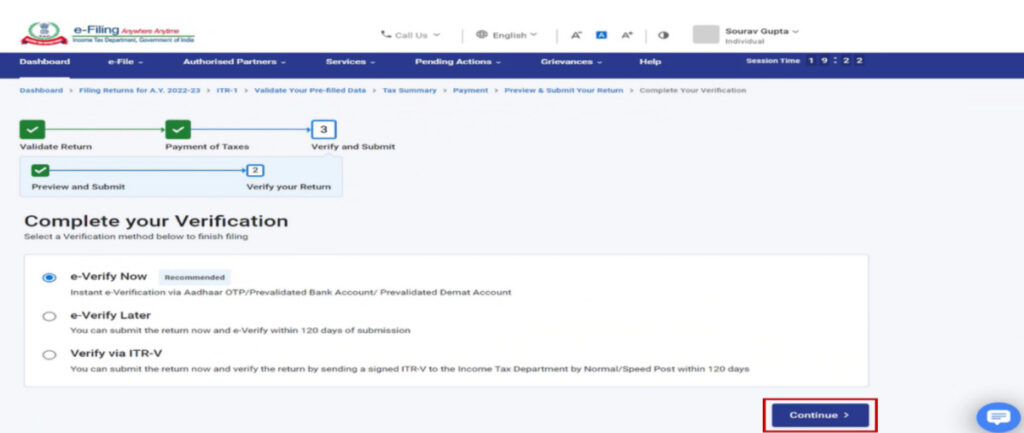

Step 17: On the ‘Complete your Verification’ page, choose your preferred option and click on “Continue.”

Note: Verifying your return is mandatory. It is recommended to opt for e-Verification. It is quick, paperless, and safer than sending a physically signed ITR-V to CPC by speed post.

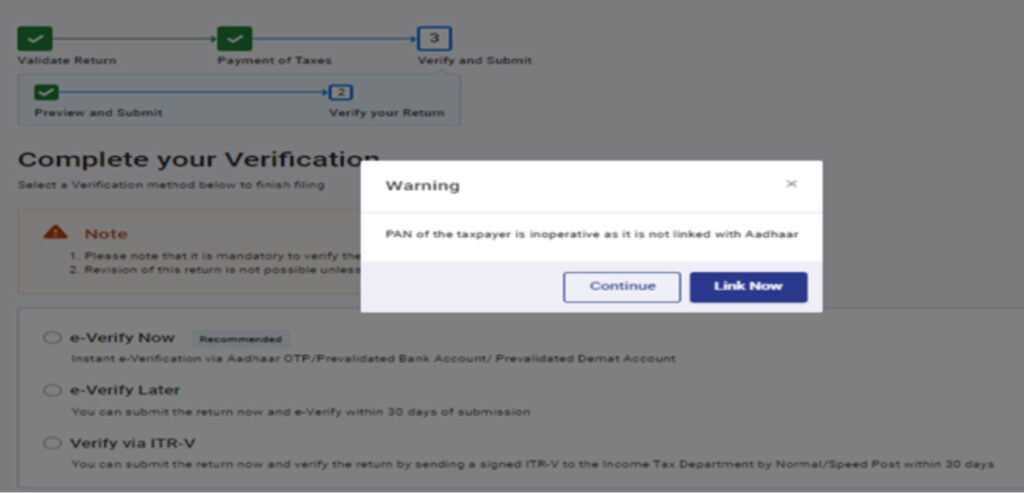

* If your PAN is inoperative and not linked with Aadhaar, a warning message will appear in a pop-up. To link your PAN with Aadhaar, click on the “Link Now” option. Otherwise, you can proceed by clicking on “Continue.”

Step 18: On the e-Verify page, choose the option that you prefer to use for e-verifying your return, and then click on “Continue“.

- If you choose the option “e-Verify Later,” you can submit your return. However, note that you will still need to verify your return within 30 days of filing your ITR.

- If you select the option “Verify via ITR-V,” remember that you need to send a signed physical copy of your ITR-V to the Centralized Processing Center, Income Tax Department, Bengaluru 560500, within 30 days using speed post.

- Make sure to pre-validate your bank account so that any refunds you are eligible for can be directly credited to your account.

- Once you successfully e-verify your return, you will see a confirmation message with the transaction ID and acknowledgement number. Additionally, you will receive a confirmation message on your registered mobile number and email ID.

Conclusion: Filing income tax is a simple process that you can do online. It involves selecting the assessment year and filing mode while providing required information such as income and deductions, reviewing tax liability or refunds, making any necessary tax payments, and verifying the return electronically. It is important to have essential documents like PAN, Aadhaar, Form 16, and bank statements ready for a smooth and accurate filing experience. This helps ensure compliance with tax obligations.

Disclaimer: This blog is written to make it easy for readers to understand complicated processes. Some information and screenshots may be outdated as government processes can change anytime without notification. However, we try our best to keep our blogs updated and relevant.