Among so many types of investment tools offered by the Indian government, General Provident Fund (GPF), Public Provident Fund (PPF), and Employee Provident Fund (EPF) are three commonly discussed options.

While they may sound similar, each serves a unique purpose and offers distinct benefits. In this comprehensive guide, we will understand the differences between GPF, PPF, and EPF, helping you understand their features and benefits. Whether you’re a government employee, a salaried individual, or just planning your financial future, understanding these schemes is crucial for making informed investment decisions.

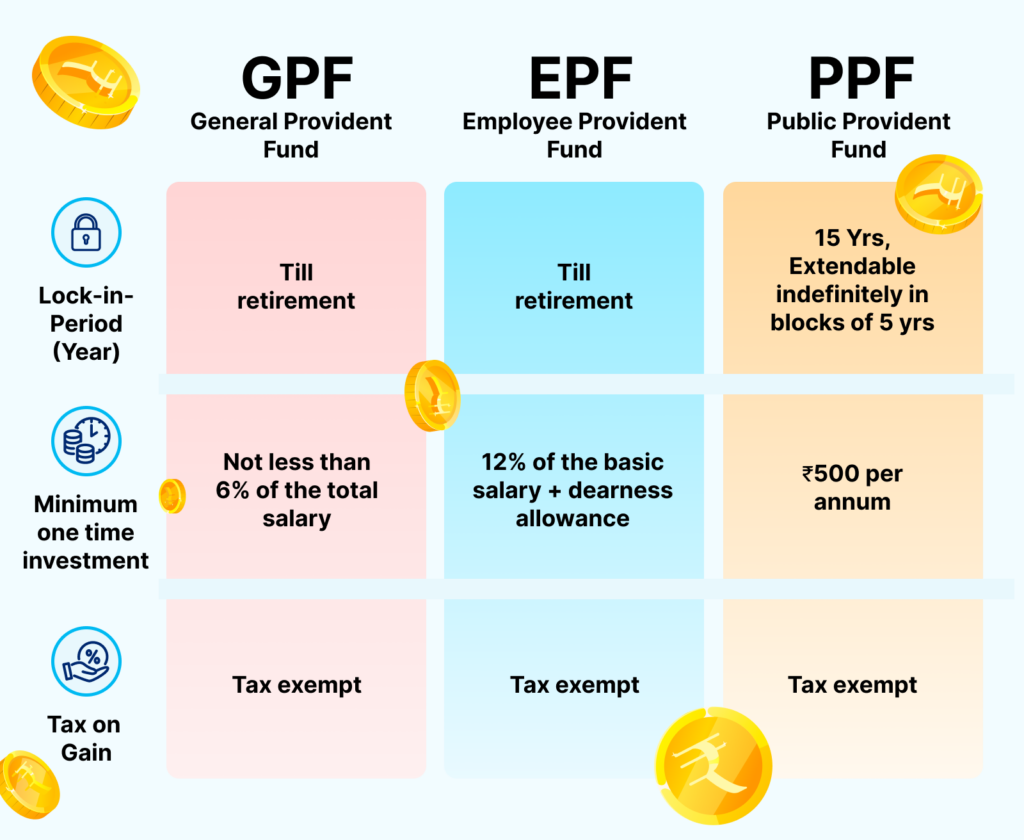

| GPF (General Provident Fund) | EPF (Employee Provident Fund) | PPF (Public Provident Fund) | |

|---|---|---|---|

| Lock-in Period | Till retirement | Till retirement | 15 years, extendable indefinitely in blocks of 5 years. |

| Minimum One-time Investment | Not less than 6% of the total salary | 12% of the basic salary + dearness allowance | Rs. 500 per annum |

| Tax on Gain | Tax-exempt | Tax-exempt | Tax-exempt |

General Provident Fund (GPF)

The General Provident Fund or GPF is a compulsory, long-term investment option for government employees. This investment option allows them to accumulate savings during their working tenure.

The scheme requires employees to contribute a certain percentage of their salary towards the fund. These contributions are deducted from their monthly salary, and the amount earns interest at a rate determined by the government.

It’s a great tax savings, low-risk investment that comes with guaranteed returns. The GPF is flexible, allowing employees to withdraw money from the fund for various reasons, such as marriage, education, and medical emergencies.

Eligibility Criteria for GPF

- Temporary government employees who have served continuously for at least one year

- Re-employed pensioners (those not eligible for CPF)

- All permanent government servants

Contribution to GPF

- The GPF contribution amount is determined by the subscriber. However, the minimum contribution should not be less than 6% of the total salary of the employee. The maximum contribution can reach up to 100% of the employee’s salary.

Tax Benefits of GPF

- Contributions made to GPF qualify for tax deductions under Section 80C of the Income Tax Act. GPF is a risk-free investment option, as it is government-backed and provides a fixed rate of return.

Employees’ Provident Fund (EPF)

The Employees’ Provident Fund (EPF) is a retirement-cum-savings scheme. Unlike GPF, EPF is mandatory for those working in an organization with more than 20 employees.

The balance in an EPF account accrues interest based on the rate set by the Employees’ Provident Fund Organisation. For the current financial year, the interest rate is set at 8.15%. This interest is calculated monthly and transferred to an individual’s EPF account at the end of every year.

Eligibility Criteria for EPF

- The employee must be part of an organization that employs a minimum of 20 individuals.

Contribution to EPF

- Both the employer and employee must contribute to the employee’s EPF account. The standard contribution from both parties is 12% of the employee’s salary (basic + dearness allowance).

Tax Benefits of EPF

- If one withdraws the balance amount from their EPF account after 5 years of account creation, it is tax-exempt. Additionally, contributions made in an EPF account every year, up to Rs. 1.5 lakh, are eligible for tax exemptions under Section 80C of the Income Tax Act, 1961.

Public Provident Fund (PPF)

The Public Provident Fund (PPF) serves as a savings scheme for anyone willing to lock in their contributions for 15 years. The interest rate on the Public Provident Fund is revised every quarter.

For the Financial Year 2024, the rate of interest on PPF has been set at 7.1%. Interest calculation under the PPF scheme is based on the lower balance between what is shown at the end of the fifth day of the month and the last day. Therefore, any deposit made after the 5th of any month is not included in the interest calculation for that month.

Eligibility Criteria for PPF

- Any resident individual who is an Indian citizen.

- Non-resident Indians (NRIs) who opened a PPF account before leaving India.

- Minors can open accounts provided their guardians/parents represent them.

Contribution to PPF

- One can make a maximum of 12 contributions per year. The minimum contribution amount is Rs. 500 annually. However, the total contribution for an individual, can’t exceed Rs. 1.5 lakh per year. This contribution aspect is a key differentiator between GPF and EPF.

Tax Benefits of PPF

- This investment is eligible for tax exemption up to Rs. 1.5 lakh under Section 80C of the Income Tax Act. Additionally, the interest earned on the balance in a PPF account, along with its maturity value, is exempt from taxation.

Let’s Simplify GPF, EPF, and PPF For You

| Features | GPF (General Provident Fund) | EPF (Employees’ Provident Fund) | PPF (Public Provident Fund) |

|---|---|---|---|

| Overview | A long-term investment scheme for government employees. | A mandatory retirement savings scheme for salaried employees. | A long-term investment scheme offered by the government. |

| Eligibility Criteria | Exclusively for government employees. | Available to employees working in organizations with 20 or more employees. | Available to all Indian citizens and HUFs. |

| Interest Rates and Returns | The interest rate is set by the government quarterly and is subject to change. | The interest rate is announced by the government annually. | The interest rate is announced by the government quarterly. |

| Withdrawal and Maturity | Withdrawal is allowed for specific purposes such as education, medical treatment, or buying a house. | Partial withdrawals are allowed for specific purposes like medical emergencies, housing, or higher education. | Partial withdrawals are allowed after the completion of the 5th financial year for specific purposes like education, medical treatment, or marriage. |

| The total balance can be withdrawn at the time of retirement or resignation. | The account can be closed at the time of retirement, resignation, or after 60 years of age. | The maturity period is 15 years, extendable indefinitely in blocks of 5 years. | |

| Tax Benefits | Contributions made to the GPF are tax-deductible under Section 80C of the Income Tax Act. | Contributions made to the EPF are tax-deductible under Section 80C of the Income Tax Act. | Contributions made to the PPF are tax-deductible under Section 80C of the Income Tax Act. |