Moving money around with just your phone has become wonderfully simple, thanks to a clever system called UPI, which stands for Unified Payments Interface. It lets you send and receive money directly from your bank account using a digital app. As you start using this handy tool, you’ll meet two important terms: a UPI ID and a UPI Number. Both are like special labels for your money, but they work in slightly different ways. Understanding each one helps you pick the best way to manage your digital cash, making everything smooth and easy.

What Exactly Is A UPI ID?

Think of a UPI ID as a special, easy-to-remember nickname for your bank account in the digital world. Instead of sharing your long account number or bank code, you can give someone this short, unique name. It’s often called a Virtual Payment Address, or VPA, and it helps keep your private bank details safe while still letting money flow to you.

Your UPI ID usually looks a bit like an email address, with letters, numbers, and an ‘@’ symbol in the middle, such as ‘your.name@bank’ or ‘yourmobile@app’. You usually pick or create this special name when you first set up your digital payment app. It’s a personal code that links directly to one of your bank accounts, making it super simple for others to send you money without needing lots of tricky details.

Where You Find Your UPI ID

Finding your own UPI ID is usually a quick task once you’ve set up your payment app and linked your bank account. It’s often displayed clearly in your app, perhaps in your profile area, under your account details, or sometimes right on the main screen. If you ever need to tell someone your ID so they can send you money, you can easily copy it from there. Knowing where your special digital name lives in your app is a good habit for any digital money user.

What Exactly Is A UPI Number?

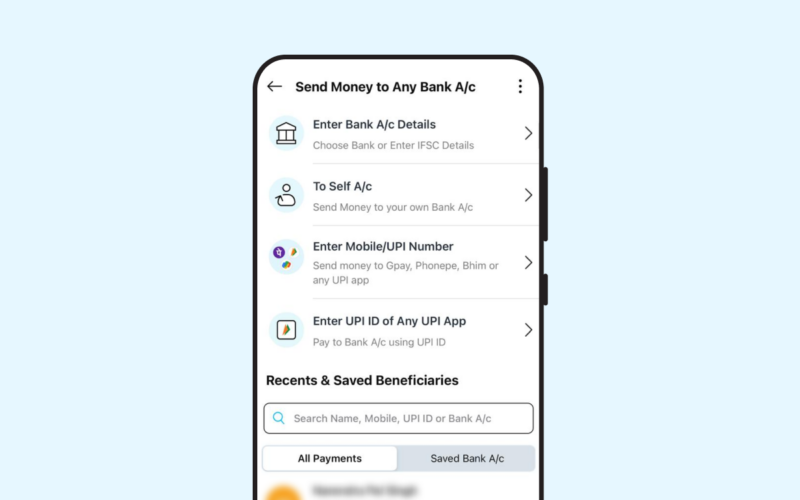

Now, let’s look at the UPI Number. This is an even more straightforward way to get money sent to you. Imagine your everyday phone number could also be your direct link to your bank account for payments – that’s what a UPI Number does! It’s usually the 8 or 10-digit mobile number you’ve told your bank about and linked to your payment app. This simpler option was created to make digital payments even easier for everyone, especially since most people already know their phone numbers by heart.

The big idea behind the UPI Number is to make sending and receiving money feel super natural. Instead of typing a mix of letters and numbers, you just use a familiar mobile number. This is incredibly useful for quick payments between friends, family, or when you’re paying a small shop where you already have their phone number saved. It cuts down on steps and makes transactions feel like a simple message.

Setting Up Your UPI Number

Getting your UPI Number ready to use is typically a very simple step. When you register for UPI through your chosen digital payment app, your registered mobile number often connects to your UPI profile automatically. If it doesn’t, or if you just want to check, you can usually find an option in the app’s settings or profile section. Look for something like “Link UPI Number” or “Register Mobile Number for UPI.” Once it’s linked, that mobile number becomes your UPI Number, allowing anyone to send money to you by simply typing it into their payment app. It’s a fast lane to digital transactions.

UPI ID Versus UPI Number: Spotting The Differences

While both a UPI ID and a UPI Number help you send and receive digital money, they are like two different tools in your toolbox, each good for different jobs. Knowing what makes them unique helps you pick the best way to handle your money for any situation.

The Main Distinction Between Them

The biggest difference is how they look and how easy they are to remember and share:

- UPI ID: This is a mix of letters and numbers, often with an ‘@’ sign in the middle (like ‘sara.smith@bank’). It’s a unique, custom name you pick for your bank account in the digital world.

- UPI Number: This is just numbers, usually your 8 or 10-digit mobile phone number that’s connected to your UPI. It’s designed to be super easy to recall and share because most people already know their phone numbers.

Think of it this way: a UPI ID is like giving your bank account a special, personalised name, while a UPI Number uses something you already use every day – your phone number – to make payments even more direct and speedy.

When You Use A UPI ID

You’ll find your UPI ID useful in several situations:

- For General Payments: When you need to send money to someone and you have their specific UPI ID.

- Receiving Payments: When you want someone to send money to you, and you share your unique UPI ID with them.

- Shop Payments: Many businesses and online shops show their UPI ID or a special picture code (QR code) for you to pay them.

- Online Shopping: When you buy things on websites or apps, you can often choose to pay using your UPI ID.

- Asking for Money: Some apps let you send a request to someone for money using their UPI ID.

It’s a flexible and safe way to handle money without telling anyone your bank account details.

When You Use A UPI Number

The UPI Number is perfect for times when you need to send money quickly and simply:

- Quick Transfers: When you want to send money fast to a friend or family member whose registered mobile number you already know.

- Receiving Money Easily: If someone wants to send you money and they have your mobile number, they can just use that to send funds straight to your linked bank account.

- Person-to-Person Payments: It’s especially handy for casual money exchanges between individuals.

- Easy to Share: It’s often much simpler to tell someone a phone number than a longer UPI ID, especially when you’re just chatting.

The UPI Number makes the payment process feel natural and quick by using an identifier you already know well.

Why Both A UPI ID And A UPI Number Are Useful

Having both a UPI ID and a UPI Number available for your digital payments is a huge bonus. It means the UPI system is adaptable, easy for everyone to use, and works well in many different situations. These options give you the power to choose the most convenient way to pay or get paid, making your money life much simpler.

Making Payments Simple and Flexible

Having both a UPI ID and a UPI Number means you have choices. You can pick the method that works best for the person you’re paying or the situation you’re in. This flexibility makes digital payments incredibly straightforward:

- Your Choice: You get to decide whether to use a custom ID or a simple phone number, depending on what feels easiest right then.

- Appeals to Everyone: It suits different preferences. Some people might like the unique, personalised feel of a UPI ID, while others find using their phone number much more direct and appealing.

- Fewer Mistakes: Having clear options for identifying who gets the money can help stop errors when sending funds, giving you more confidence with each transaction.

This two-way approach ensures UPI is a truly welcoming payment system for all.

Adding An Extra Layer of Convenience for You

Beyond just being simple and flexible, having both options makes your digital payment experience much more convenient:

- Effortless Sharing: You can share your UPI ID for more formal or varied transactions, or simply give your mobile number (your UPI Number) for quick, personal money transfers, depending on what feels right.

- Better Security: Both methods ensure that your sensitive bank account details stay private. You never have to share your actual account number or bank code with anyone directly.

- Wider Use: By offering clear and diverse options, UPI encourages more people to try digital payments, making transactions faster and more efficient for everyone involved.

- More Control: Ultimately, these options give you more power and convenience over how you manage and move your money digitally, fitting smoothly into your everyday life.