Managing your money well is an essential life skill, and it often starts with understanding the different tools available to you. When it comes to bank accounts, two main types you’ll hear about are savings accounts and current accounts. Both are highly beneficial, but they serve different purposes, especially when you use modern payment methods like UPI. Knowing the differences can help you make smart choices about where you keep your money and how you use it every day.

Getting Started: What Are Bank Accounts and Why Do They Matter?

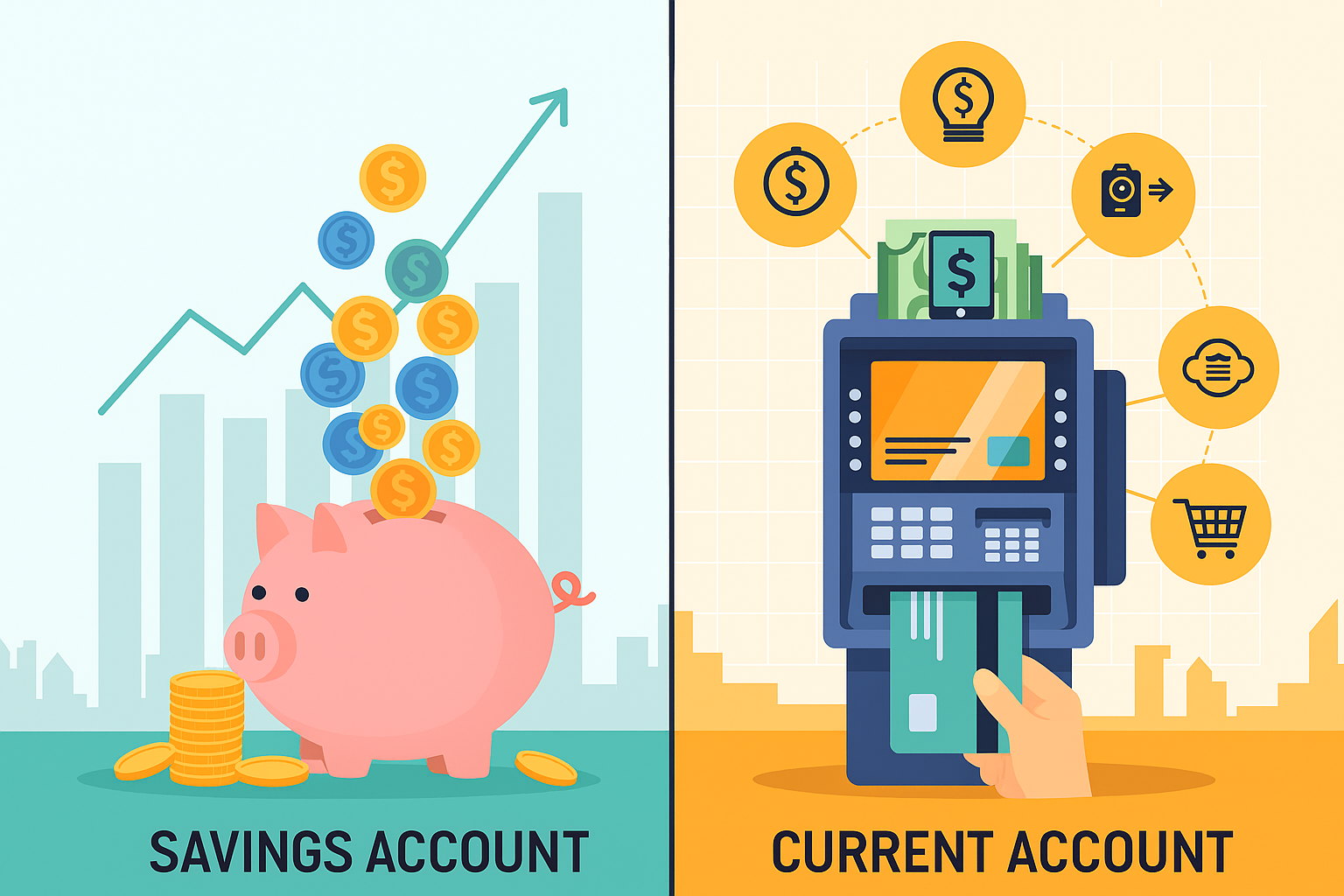

Your Money’s Home: Why We Use Bank Accounts

Think of a bank account as a safe and organised home for your money. Instead of keeping all your cash under your bed or in a jar, you deposit it into a bank. Banks are trusted institutions that safeguard your funds, keep them secure, and help you manage them easily. They allow you to send money to others, receive payments, and even save up for big purchases or your future. Having a bank account makes your financial life much simpler and safer.

Exploring Your Savings Account

What Exactly is a Savings Account?

A savings account is designed for you to keep money that you intend to save for future use. It’s like a dedicated fund where you put money aside for your goals, whether that’s buying something special, going on holiday, or preparing for unexpected events. It’s perfect for individuals and families who want a secure place to store their funds and watch them grow.

Helping Your Money Grow: How Savings Accounts Earn Interest

One of the best things about a savings account is that your money can accrue interest and grow over time. Banks usually pay you a return on your deposit, called ‘interest’, for keeping your funds with them. This means that the longer your money stays in your savings account, the more it can increase, making it a smart choice for long-term financial planning.

Keeping Your Money Safe: The Main Purpose of Saving

The primary purpose of a savings account is to provide a secure environment for your funds. Banks have strong security measures in place to safeguard your deposits against theft or loss. It gives you peace of mind knowing your hard-earned money is secure while you’re not using it.

How Often Can You Use Your Savings Account? Understanding Transaction Limits

While savings accounts are great for keeping money safe and earning interest, they are not primarily intended for high-frequency transactions. Banks usually set limits on how many times you can withdraw money or make payments from your savings account each month without incurring additional fees. This encourages you to use it for saving rather than for everyday spending.

Using UPI with Your Savings Account: Everyday Payments Made Easy

Even with transaction limits, your savings account is well-suited for using UPI (Unified Payments Interface) for your daily, personal payments. You can link your savings account to your UPI application and easily send money to friends, family, or pay for groceries, utility bills, or online shopping. It’s a quick and simple way to handle your routine expenses directly from your saved funds.

Exploring Your Current Account

What Exactly is a Current Account?

A current account is distinctly different from a savings account. It’s designed for individuals or businesses that need to make and receive payments very frequently throughout the day. Think of it as a busy hub where money is constantly flowing in and out.

For Businesses and Busy Transactions: Why Current Accounts Are Different

Current accounts are primarily utilized by businesses, self-employed individuals, and organisations. They need to handle numerous daily transactions, such as paying suppliers, receiving money from customers, or managing payroll. A current account provides the flexibility and capacity for this high volume of activity.

Focus on Convenience, Not Interest: A Key Feature

Unlike savings accounts, current accounts typically do not accrue interest on the money held within them. The main benefit of a current account is the convenience of high transaction volumes and often unlimited transactions. It prioritises ease of access and frequent money movement over earning a return on your balance.

A Helping Hand for Businesses: Understanding Overdraft Facilities

Many current accounts come with an ‘overdraft’ facility. This means that if a business needs to make a payment but has insufficient funds in its account, the bank might allow them to withdraw funds exceeding their current balance, up to a pre-agreed limit. This can be a beneficial short-term solution for managing cash flow, though it usually comes with fees or interest charges.

Using UPI with Your Current Account: Managing Business Payments

For businesses, linking a current account to UPI is highly advantageous. It allows for quick and efficient business transactions. You can easily pay vendors, receive payments from clients, or manage other operational expenses directly through UPI, ensuring smooth and fast financial operations.

Key Differences in How You Use UPI

Why Your Account Type Matters for UPI

The type of bank account you link to your UPI application significantly affects how you use it. It’s not just about making payments; it’s about the purpose and volume of those payments.

How Much You Can Send and Receive: Transaction Volume

While UPI generally has daily transaction limits set by the National Payments Corporation of India (NPCI) and individual banks, the intended volume of transactions differs between account types. Savings accounts are typically for personal, lower-volume use, whereas current accounts are designed to handle a much higher frequency and often larger sums of money, which is crucial for business operations.

Personal vs. Business Needs: The Purpose of Your Payments

- Savings Account UPI: Best for personal expenses, sending money to friends or family, paying small bills, and everyday shopping.

- Current Account UPI: Ideal for business-related payments, receiving customer payments, paying employees, and managing various commercial transactions.

Interest Earnings: A Major Distinction Between Account Types

Remember, a key difference is that your savings account can earn interest, helping your money grow, while a current account typically does not. This fundamental distinction influences which account is better suited for your specific financial goals.

Choosing the Right Account for You

When a Savings Account is Your Best Friend

- An individual looking to save money for the future.

- Someone who makes occasional payments and withdrawals.

- Seeking to earn interest.

- Primarily using your account for personal expenses and financial goals.

When a Current Account Makes More Sense for Your Needs

- Operating a business, regardless of size.

- A self-employed professional with frequent transactions.

- Requiring frequent daily transactions for payments and receipts.

- Looking for an account that offers overdraft facilities for cash flow management.

Important Things to Remember About UPI

Keeping Your UPI Transactions Safe and Secure

UPI is a highly secure method to make payments, but you also bear responsibility for ensuring the security of your funds. Always remember to:

- Never share your UPI PIN with anyone, including bank officials.

- Check the recipient’s details carefully before confirming a payment.

- Use a strong screen lock and password for your phone.

- Exercise caution regarding suspicious links or requests for your PIN, especially if told it is to ‘receive’ money. Remember, a UPI PIN is only required to send money.

Understanding UPI Limits for Different Account Types

It’s important to know that there are daily and per-transaction limits for UPI payments, which are set by NPCI and your specific bank. While these limits are generally sufficiently accommodating for personal use, businesses using current accounts might have different considerations or need to manage their transactions within these frameworks. Always check with your bank for the most up-to-date information on UPI transaction limits for your particular account type to ensure smooth operations.