Losing a cheque is like misplacing your house keys; you know they are somewhere, but until found, your home is not fully secure. Similarly, a lost or stolen cheque can expose your bank account to significant risks, making quick action essential.

Understanding the difference between a stop payment and a cancellation is crucial for protecting your finances. You need to act swiftly and correctly to prevent potential fraud or financial loss from unauthorised transactions.

A stop payment request is an official instruction given to your bank to prevent a specific cheque from being paid, even if presented for encashment. This process is governed by Reserve Bank of India (RBI) guidelines and your bank’s specific policies, requiring you to provide details like the cheque number and amount.

Cheque cancellation, on the other hand, involves making a cheque invalid when it is still in your possession, often by writing “Cancelled” across it. If a cheque is lost or stolen and you fail to issue a stop payment, an unauthorised person could potentially cash it, leading to significant financial loss from your account.

Your bank typically processes stop payment requests within minutes, though a fee may apply as per their latest official guidelines. You should contact your bank’s customer service or visit a branch immediately to protect your funds.

Table of Contents

Understanding Your Cheque Book

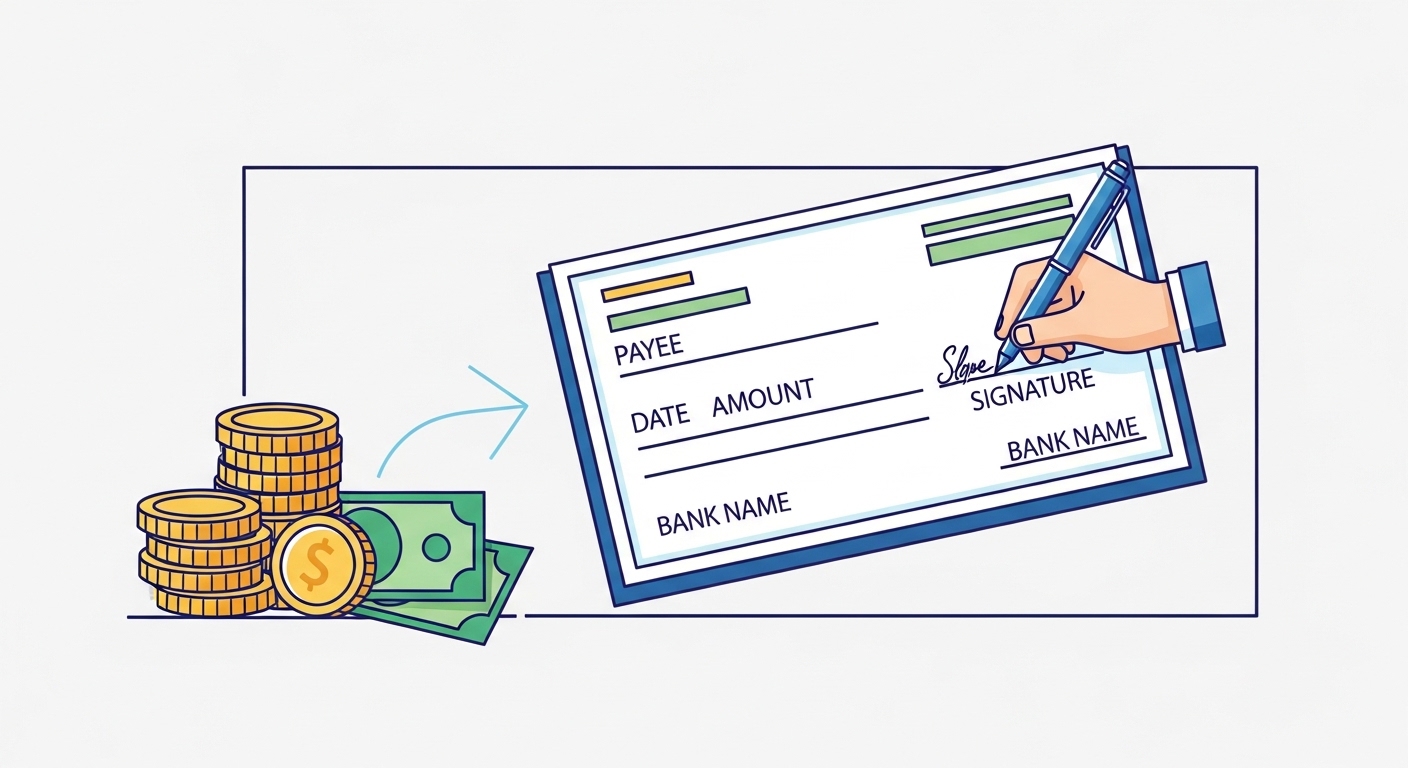

A cheque book is a vital tool for managing your finances, allowing you to make payments without needing physical cash. It’s important to understand how cheques work and what each part means for secure transactions. These physical payment instruments still play a significant role in various financial dealings across India, despite the rise of digital payments.

Knowing the components of a cheque helps you use them correctly and identify potential issues. Each section serves a specific purpose, from identifying your bank to authorising the payment itself. Keeping your cheque book safe is just as important as protecting your debit card or online banking credentials.

What is a cheque?

A cheque is a written, unconditional order addressed to a bank, signed by the drawer, directing the bank to pay a specified sum of money to a particular person or the bearer of the instrument. It is essentially a promise of payment from your bank account. This traditional payment method remains important for large transactions, government payments, and situations where digital transfers are not feasible.

Parts of a cheque

Every cheque contains several key pieces of information that ensure it can be processed correctly. Familiarising yourself with these parts helps you fill them out accurately and understand the data required for a stop payment. Incorrect details can lead to a cheque being dishonoured or a stop payment request being delayed.

- Date: The date on which the cheque is written, which determines its validity period.

- Payee Name: The name of the person or entity to whom the payment is being made.

- Amount in Words: The payment amount written out in words to prevent alteration.

- Amount in Figures: The payment amount written numerically, matching the words.

- Account Number: Your bank account number from which the funds will be debited.

- Cheque Number: A unique six-digit number identifying the specific cheque.

- MICR Code: A nine-digit Magnetic Ink Character Recognition code for bank and branch identification.

- IFSC Code: The Indian Financial System Code for electronic funds transfer.

- Signature: Your authorised signature, validating the payment instruction.

Why cheques are important

Cheques offer a traceable and formal method of payment, often preferred for large sums or official transactions. They provide a physical record of payment, which can be useful for accounting and legal purposes. While digital options like UPI and IMPS are quick, cheques still serve a crucial function in India’s diverse payment landscape.

Quick Context: Cheque Validity

A cheque is typically valid for three months from its date of issue. After this period, it becomes a “stale cheque” and your bank will not honour it.

What Happens If a Cheque Goes Missing?

A lost or stolen cheque poses a serious threat to your financial security, far beyond just the amount written on it. It can lead to unauthorised withdrawals, identity theft, and significant hassle as you try to recover your funds. Understanding these risks is the first step towards protecting yourself effectively.

Acting quickly is not just a recommendation; it’s a necessity when a cheque goes missing. Every moment that passes increases the potential for misuse, so you must know the immediate steps to take. Your bank needs to be informed as soon as possible to prevent any fraudulent activity.

Risks of a lost cheque

If a blank cheque is lost, someone could fill it out for any amount and attempt to cash it. Even if it is a filled-out cheque, an unauthorised person might try to alter the payee’s name or amount. This can lead to your account being debited without your permission, causing immediate financial loss.

Dangers of a stolen cheque

A stolen cheque carries even greater risks, as it often implies malicious intent. Thieves might try to forge your signature or use the cheque details to commit identity fraud. They could also attempt to create duplicate cheques using your account information, opening up a wider range of fraudulent activities.

Act quickly to protect yourself

The moment you realise a cheque is lost or stolen, you must contact your bank without delay. This prompt action can be the difference between a minor inconvenience and a major financial setback. Delaying could mean that the cheque is presented and cleared before you can stop the payment.

Pro Tip: Keep a Cheque Register

Always maintain a record of all cheques issued, including the cheque number, date, payee, and amount. This information is critical if you ever need to request a stop payment.

What Is a Stop Payment Request?

A stop payment request is a formal instruction you give to your bank to prevent a specific cheque from being honoured. This instruction ensures that even if the cheque is presented for payment, your bank will not release the funds from your account. It’s a critical tool when a cheque is no longer supposed to be paid.

This action is most effective when the cheque has not yet been presented to your bank for clearing. Once funds have left your account, a stop payment request becomes irrelevant for that particular transaction. You must therefore act before the cheque reaches your bank’s processing system.

Your bank will then block any attempts to encash that specific cheque number. This protective measure is designed to safeguard your funds from misuse or from being paid out incorrectly. It’s a powerful way to regain control over a payment that has gone astray.

Stopping a cheque’s payment

When you initiate a stop payment, you are essentially telling your bank to invalidate that cheque number in its system. This means that if anyone tries to present that cheque, the bank will reject it. This is a crucial step to take if you suspect fraud or if a payment needs to be halted.

When money has not left

A stop payment request is most effective when the funds are still in your account and the cheque has not been cleared. If the cheque has already been debited from your account, you would typically need to explore other options like a dispute resolution process. Therefore, timing is absolutely key for this action.

Your bank blocks payment

Upon receiving your request, your bank immediately places a block on the specific cheque number. This prevents any future attempts to cash or deposit it. You will usually receive a confirmation from your bank that the stop payment has been successfully registered.

Common Confusion: Stop Payment Duration

It is commonly assumed that a stop payment request lasts forever

Most banks set a validity period, often six months, after which the stop payment expires. You may need to renew it if the risk persists beyond this period, as per bank guidelines.

When Should You Request a Stop Payment?

Knowing when to issue a stop payment request is as important as knowing how to do it. There are specific scenarios where this action is the most appropriate and effective way to protect your funds. Acting decisively in these situations can prevent significant financial complications.

This tool is designed for situations where a cheque has left your physical possession but should no longer be paid. It’s a defensive measure to prevent an unintended transfer of funds. Always consider the reason behind stopping the payment to ensure it’s the right course of action.

- Cheque lost before delivery: If you’ve mailed a cheque and it gets lost in transit, a stop payment prevents it from being cashed by an unintended recipient.

- Cheque stolen from you: If your cheque book or a specific cheque is stolen, immediately requesting a stop payment protects your account from fraudulent use.

- Incorrect amount written: If you realise you’ve written the wrong amount on a cheque after handing it over, a stop payment can prevent the incorrect sum from being debited.

- Dispute with the payee: If you’ve issued a cheque for goods or services, but a dispute arises before the cheque is cleared, you might request a stop payment. However, be aware of the legal implications of stopping payment on a valid debt.

Pro Tip: Verify Delivery Status

If you’ve sent a cheque by post, try to verify its delivery status. If it shows as undelivered or lost, act immediately to place a stop payment.

How Do You Request a Stop Payment?

Requesting a stop payment is a time-sensitive process that requires immediate action and accurate information. You must follow your bank’s specific procedures to ensure the request is processed effectively. Preparing all necessary details beforehand will make the process smoother and faster.

Most banks offer multiple channels for initiating a stop payment, including online banking, mobile apps, phone banking, or visiting a branch. Choose the quickest method available to you, especially if time is of the essence. Remember that a fee may be applicable for this service, as per your bank’s official guidelines.

Step 1: Contact your bank promptly.

As soon as you realise a cheque is lost or stolen, call your bank’s customer service helpline or visit your nearest branch immediately. Inform them about the situation and state your intention to place a stop payment.

Step 2: Provide cheque details.

You will need to furnish specific information about the cheque, including the cheque number, the amount, the date it was issued, and the payee’s name (if known). Having your bank account number and personal identification ready will also speed up the process.

Step 3: Fill out a form.

Many banks require you to fill out a physical or digital stop payment request form. Ensure all details are accurate and sign it if required. This form serves as your official instruction to the bank.

Step 4: Understand any fees.

Your bank may levy a service charge for processing a stop payment request. Inquire about the exact fee at the time of your request. This fee can vary between banks and is subject to their latest official guidelines.

Hover to preview each step · Click to pin the details open

Common Confusion: Stop Payment Guarantee

The misunderstanding here is that a stop payment guarantees no funds will ever leave your account

While highly effective, if the cheque is presented and cleared before your bank processes the stop payment, it may still be honoured. Immediate action is critical.

What Is Cheque Cancellation?

Cheque cancellation is a straightforward process that makes a cheque invalid when it is still in your possession. This action prevents the cheque from ever being used for payment. It's a simple yet effective way to nullify a cheque that you no longer intend to use.

You typically cancel a cheque when you have made a mistake on it, or the underlying transaction is no longer going forward. Unlike a stop payment, cancellation happens before the cheque leaves your hands. This means there's no risk of it being misused by someone else.

By cancelling a cheque, you are ensuring it cannot be presented for payment at any point in the future. This provides peace of mind and prevents potential complications. It's a proactive measure to manage your cheque book responsibly.

Making a cheque invalid

The primary goal of cancellation is to render a cheque unusable. This is usually done by writing "Cancelled" prominently across the face of the cheque. This clear marking ensures that no bank will accept it for processing.

When you have the cheque

Cancellation is only possible when the cheque is physically with you. If the cheque has left your possession, even inadvertently, you should consider a stop payment instead. The ability to physically mark the cheque is key to this process.

Preventing future use

Once cancelled, the cheque cannot be misused, even if it falls into the wrong hands. It serves as a permanent record that the cheque was never intended for payment. This simple step can save you from future headaches and potential fraud.

Quick Context: Cheque Book Safety

Always keep your cheque book in a secure location, treating it with the same care as your cash or debit cards. Never leave it unattended or in easily accessible places.

When Should You Cancel a Cheque?

Cancelling a cheque is the appropriate action when you still have physical control over it and no longer wish for it to be used. This differs significantly from a stop payment, which is for cheques that have left your possession. Understanding these scenarios helps you choose the right protective measure.

This action is a preventive step, ensuring that a cheque you no longer need or that contains errors cannot be accidentally or intentionally misused. It's about maintaining control over your financial instruments. Always double-check your intentions before cancelling.

- Cheque made a mistake: If you've written the wrong date, amount, or payee name on a cheque, it's best to cancel it and issue a new one. This prevents potential issues during clearing.

- Transaction no longer happening: If you prepared a cheque for a payment that is now cancelled or no longer required, you should cancel the cheque. This ensures the funds remain in your account.

- Cheque is still with you: The fundamental condition for cancellation is that you physically possess the cheque. If it's lost or stolen, cancellation is not an option; a stop payment is needed.

Pro Tip: Mark Clearly

When cancelling a cheque, write "CANCELLED" in large, clear letters across the entire face of the cheque, ensuring it cannot be overlooked or altered.

How Do You Cancel a Cheque?

Cancelling a cheque is a simple, two-step process that you can perform yourself. It ensures the cheque is permanently invalidated and cannot be used for any transaction. This method is effective because it physically marks the cheque as unusable.

While the primary action is marking the cheque, it's also wise to inform your bank for record-keeping purposes. This adds an extra layer of security and ensures your bank is aware of the invalidated instrument. Always maintain good records of your cancelled cheques.

Step 1: Write "Cancelled" clearly.

Take the physical cheque and write the word "CANCELLED" in large letters across the entire face of the cheque. Make sure it crosses the payee line, amount boxes, and signature area to prevent any part from being used.

Step 2: Inform your bank.

While not always strictly mandatory for cancellation, it's good practice to inform your bank about the cancelled cheque. This helps them update their records and provides an additional layer of security, especially if the cheque number was previously recorded for a transaction.

Step 3: Keep a record.

Retain the cancelled cheque safely with your other financial documents. This serves as proof that the cheque was intentionally invalidated. You might also note the cancellation in your cheque book register.

Hover to preview each step · Click to pin the details open

Common Confusion: Bank Notification for Cancellation

A widespread myth is that you must always notify your bank when you cancel a cheque

While advisable for record-keeping, physically marking "CANCELLED" on a cheque you possess is usually sufficient to invalidate it. Your bank cannot honour a visibly cancelled cheque.

Read More

How to approve UPI payment in Paytm?Key Differences: Stop Payment Versus Cancellation

Understanding the distinct differences between a stop payment and a cheque cancellation is crucial for effective financial protection. While both actions aim to prevent a cheque from being paid, they apply to entirely different situations and involve different processes. Misapplying one for the other can lead to further complications or leave your account vulnerable.

The primary distinction lies in who has possession of the cheque and the specific purpose of the action. One is a reactive measure for a cheque that has left your control, while the other is a proactive step for a cheque still with you. Knowing when to use each is key to managing your cheque-based transactions securely.

| Feature | Stop Payment | Cancellation |

| Cheque Possession | Cheque is lost, stolen, or issued to payee | Cheque is still with you |

| Purpose | To prevent payment of an issued/missing cheque | To invalidate a cheque before issue or due to error |

| Action By | Bank, upon your request | You, by marking the cheque |

| Timing | After cheque has left your possession | Before cheque leaves your possession |

| Fees | Often applicable, as per bank guidelines | Generally no fee |

| Example | Lost cheque in mail, stolen cheque book | Mistake made while writing cheque, transaction cancelled |

Pro Tip: Choose Wisely

Always assess whether the cheque is still in your physical possession. If yes, cancel it.

If no, initiate a stop payment immediately. This simple rule guides your decision.

Important Things to Remember

When dealing with lost or stolen cheques, or even just errors, several key principles will guide you towards the best outcome. These points are not just procedural steps but essential safeguards for your financial well-being. Keeping them in mind helps you act responsibly and effectively.

Your vigilance and promptness are your best defence against potential fraud or financial loss. Never underestimate the importance of timely action and meticulous record-keeping. These habits form a strong foundation for secure financial management.

- Time is very important: The faster you act after realising a cheque is lost or stolen, the higher the chance of preventing fraudulent activity. Delays can be costly and difficult to reverse.

- Keep all records: Always retain copies of your stop payment requests, acknowledgement slips, and any communication with your bank. This documentation is vital proof if a dispute arises.

- Understand bank charges: Be aware that your bank may charge a fee for a stop payment request. Inquire about these charges upfront so there are no surprises.

- Seek bank assistance: Don't hesitate to contact your bank for guidance. Their customer service representatives can provide specific instructions and support tailored to your situation.

Quick Context: Digital Payment Alternatives

For many routine transactions, digital payment methods like UPI, IMPS, and Bharat BillPay offer instant, traceable, and often more secure alternatives to cheques. According to NPCI (2026), UPI has become a cornerstone of India's digital economy, facilitating billions of transactions annually.

Protecting Your Money and Information

Beyond specific actions like stop payments or cancellations, adopting robust security practices for your cheques and bank information is paramount. Proactive measures can significantly reduce your risk of becoming a victim of fraud. Your financial security largely depends on your daily habits.

Regularly reviewing your bank statements and being cautious with your personal details are simple yet powerful ways to protect yourself. These practices help you spot unusual activity quickly and prevent small issues from escalating into major problems. Always be alert to anything that seems out of the ordinary.

- Be careful with cheques: Store your cheque book in a secure, locked place at home. Never pre-sign blank cheques, and always fill out all details before handing over a cheque.

- Check your bank statements: Regularly review your bank account statements for any unauthorised or suspicious transactions. The sooner you spot an anomaly, the easier it is to address it.

- Report suspicious activity: If you notice any unusual activity related to your bank account or cheques, report it to your bank immediately. Early reporting is crucial for investigation and recovery.

Common Confusion: Cheque Details Safety

The belief is that sharing your cheque number is harmless if you don't share your signature - but this is incorrect.

Even without your signature, a cheque number, account number, and IFSC code can be used in various fraud schemes, including creating fake cheques or phishing attempts.