Are you struggling with multiple debts and unsure of how to achieve financial freedom? Don’t worry, there are two effective methods to help you repay your debts: the Snowball Method and the Avalanche Method. With the avalanche method, you pay off the debt with the highest interest rate first. However, with the snowball method, you start by paying off the smallest debt first. For both methods, you list all your debts and make minimum payments on everything except the debt you’re focusing on. Once that debt is cleared, you move on to the next one, continuing until all your debts are paid.

In this blog, we will explain these methods in detail and discuss the differences between them. By understanding the strategies of each approach, you can make an informed decision that suits your financial goals and personal preferences.

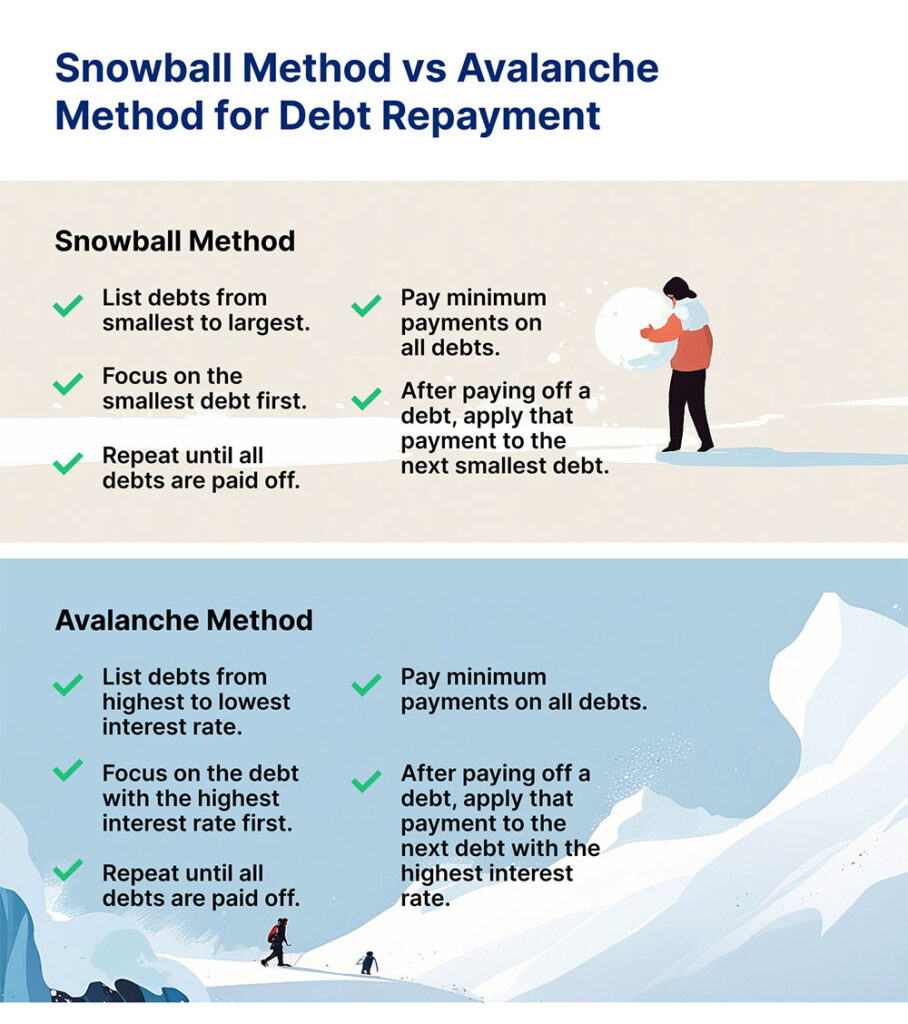

What is Snowball Method for Debt Repayment?

The Snowball Method is a popular strategy for effectively tackling multiple debts. It gets its name from the idea of starting small and gradually gaining momentum, just like a snowball rolling downhill and accumulating more snow. With this method, you begin by paying off your smallest debts first and then move on to larger ones.

How does the Snowball Method Work?

- List your debts: Make a list of all the debts you have, like credit cards, personal loans, or car loans. Write down how much you owe, the interest rates, and the minimum monthly payments for each debt.

- Order debts by size: Arrange your debts from smallest to largest based on the amount you owe. The smallest debt should be at the top of the list, and the largest debt at the bottom.

- Make minimum payments: Keep making the minimum monthly payments on all your debts to avoid any penalties or fees.

- Focus on the smallest debt: Take any extra money you can afford and put it towards paying off the smallest debt. Try to pay it off as quickly as possible.

- Snowball effect: Once the smallest debt is paid off, take the money you were using to pay that debt (minimum payment + extra money) and add it to the minimum payment of the next smallest debt. This creates a snowball effect, where your payments towards the next debt become larger.

- Repeat the process: Keep following this process of paying off one debt at a time and using the money you save to pay off the next one. As you cross off each debt from your list, you’ll have more money available to tackle the larger debts.

Consider the following example to understand snowball method better:

Let’s say you have three debts:

- Credit Card A: ₹10,000 balance with a minimum payment of ₹500 and an interest rate of 18%.

- Student Loan B: ₹50,000 balance with a minimum payment of ₹1,000 and an interest rate of 6%.

- Car Loan C: ₹1,00,000 balance with a minimum payment of ₹2,000 and an interest rate of 4%.

Using the Snowball Method, you start by focusing on the smallest debt, which is Credit Card A. You make the minimum payment of ₹500, but you also allocate an additional ₹1,500 from your budget to pay off this debt faster, making a total payment of ₹2,000 per month.

After a few months of consistent payments, you successfully pay off Credit Card A in, let’s say, 6 months. Now, instead of paying ₹2,000 towards Credit Card A, you roll that amount into the next debt, Student Loan B. So, for Student Loan B, you’re making the minimum payment of ₹1,000 plus the additional ₹2,000 from the paid-off credit card debt, resulting in a total payment of ₹3,000 per month.

Continuing with this approach, you make ₹3,000 monthly payments towards Student Loan B until it is fully paid off. Let’s say it takes you 18 months to clear this debt.

Once Student Loan B is paid off, you move on to the last debt, Car Loan C. Now, you allocate the minimum payment of ₹2,000 from the student loan and add it to the ₹3,000 you were already paying for a total payment of ₹5,000 per month towards Car Loan C.

Pros and Cons of Snowball Method

| Pros | Cons |

|---|---|

| Helps build motivation by paying off smaller debts quickly | Doesn’t reduce interest costs as effectively as the debt avalanche method |

| May take longer to pay off all debts completely |

What is Avalanche Method for Debt Repayment?

The Avalanche Method is another popular strategy for paying off multiple debts efficiently. Unlike the Snowball Method, which focuses on the smallest debts first, the Avalanche Method prioritizes debts based on their interest rates. The goal is to minimize the total amount of interest paid over time by paying off the most expensive debts first.

How Does the Avalanche Method Work?

- List your debts: Write down all your debts, including the balance, interest rate, and minimum monthly payment for each one.

- Order debts by interest rate: Arrange your debts from highest to lowest interest rate. The debt with the highest interest rate goes on top, and the one with the lowest interest rate goes at the bottom.

- Make minimum payments: Make sure you pay at least the minimum amount required for each debt every month. This avoids extra fees or penalties.

- Focus on the highest-interest debt: Use any extra money you have to pay off the debt with the highest interest rate.

- Move down the list: Once you’ve paid off the highest interest debt, take the money you were using for it (minimum payment + extra money) and add it to the minimum payment of the next debt with the highest interest rate. This helps you pay off the next debt faster.

- Repeat the process: Keep going through the list, paying off one debt at a time, and adding the payments to the next debt. This way, you’ll pay off the debts with higher interest rates first, saving you money in interest charges over time.

Consider the following example

Let’s say you have three debts:

- Credit Card A: ₹10,000 balance with an interest rate of 18%.

- Student Loan B: ₹50,000 balance with an interest rate of 6%.

- Car Loan C: ₹1,00,000 balance with an interest rate of 4%.

Using the Avalanche Method, you start by prioritizing the debt with the highest interest rate, which is Credit Card A at 18%.

You make the minimum payment of, let’s say, ₹500 towards Credit Card A, but you allocate an additional ₹2,000 from your budget to pay off this debt faster, making a total payment of ₹2,500 per month.

After a few months of consistent payments, you successfully pay off Credit Card A. Now, instead of paying ₹2,500 towards Credit Card A, you roll that amount into the next debt, which is Student Loan B.

For Student Loan B, you continue making the minimum payment of, let’s say, ₹1,000, but now you add the ₹2,500 from the paid-off credit card debt, resulting in a total payment of ₹3,500 per month.

Continuing with this approach, you make ₹3,500 monthly payments towards Student Loan B until it is fully paid off.

Once Student Loan B is paid off, you move on to the last debt, Car Loan C. Now, you allocate the minimum payment of, let’s say, ₹2,000 from the student loan and add it to the ₹3,500 you were already paying for a total payment of ₹5,500 per month towards Car Loan C.

Pros and Cons of Avalanche Method

| Pros | Cons |

|---|---|

| Lowers the total interest paid over time | Requires strong discipline and commitment |

| Helps you become debt-free faster | Works best if you have extra money to put toward payments |

| Ideal for people who prioritize long-term savings |

Difference between Snowball and Avalanche Methods

| Method | Snowball Method | Avalanche Method |

|---|---|---|

| Priority | Focus on small debts first | Focus on high-interest debts first |

| Ordering | List debts from smallest to largest | List debts from highest to lowest interest |

| Motivation | Feel accomplished, eliminate small debts quickly | Aim to save money by reducing overall interest |

| Strategy | Pay the minimum on all, extra to the smallest debt | Pay minimum, extra to highest interest |

| Benefits | Boost morale, stay motivated | Save money on interest in the long run |

Ultimately, the choice between the Snowball Method and the Avalanche Method depends on your personal preferences and financial situation. If you value quick wins and psychological motivation, the Snowball Method may be more suitable. However, if you prioritize saving on interest payments and want to tackle high-interest debts first, the Avalanche Method may be a better fit. Consider your financial goals, interest rates, and personal motivation to determine which method aligns best with your needs.

Disclaimer: Nothing on this blog constitutes investment advice, performance data or any recommendation that any security, portfolio of securities, investment product, transaction or investment strategy is suitable for any specific person. You should not use this blog to make financial decisions. We highly recommend you seek professional advice from someone who is authorised to provide investment advice.