Life can feel quite complicated sometimes, especially when it comes to managing your money. You might have seen your parents or other adults using cheques, those little paper slips that seem to hold a lot of power. It’s easy to feel a bit lost or worried about making a mistake when dealing with something so important, and an error could lead to unnecessary stress or even financial trouble.

Thankfully, understanding how cheques work doesn’t have to be a mystery. By learning a few simple rules and being careful, you can confidently use cheques for various payments, ensuring your money goes exactly where it’s supposed to. This guide will walk you through everything you need to know, making you a master of this traditional yet still very useful payment method.

What Is a Cheque and Why Do We Use It?

Understanding this payment method

A cheque is simply a piece of paper that tells your bank to pay a certain amount of money from your account to another person or company. Think of it as a written instruction or a command you give to your bank. When you write a cheque, you’re essentially saying, “Dear Bank, please take this much money out of my account and give it to the person whose name I’ve written here.”

Why cheques are useful

Even in today’s digital world, cheques remain a very useful payment tool for many reasons. They offer a clear record of your transactions, which can be helpful for budgeting or when you need proof of payment. For larger amounts of money, or when you’re paying someone who might not have a digital payment setup, cheques provide a safe and widely accepted option. They’re also a great way to pay bills or transfer money when you don’t want to carry a lot of cash around.

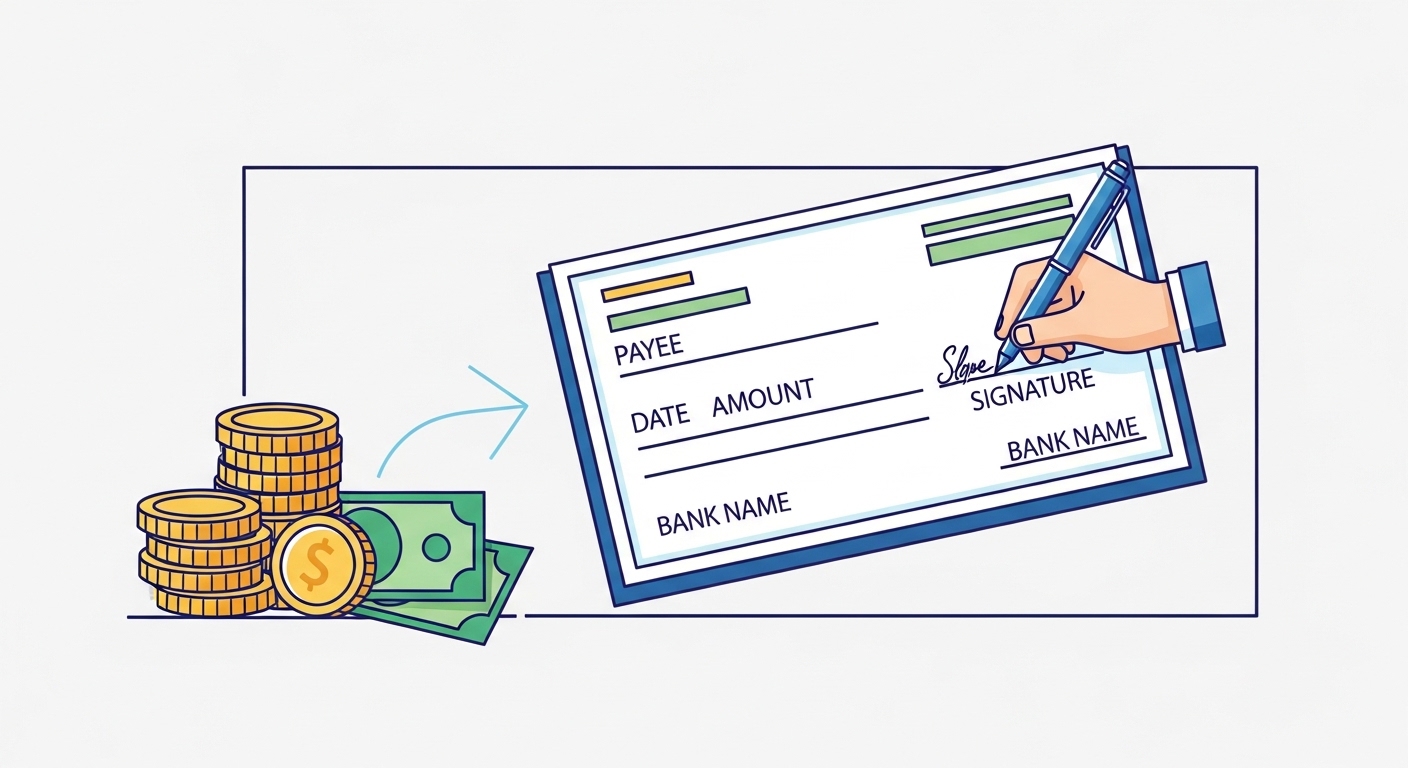

Getting to Know the Parts of Your Cheque

Before you start writing, it’s really important to know what each part of a cheque means. Each section has a specific purpose and helps ensure your payment is processed correctly and safely.

Your bank’s name

You’ll find your bank’s name and logo printed clearly at the top of the cheque. This tells everyone which bank holds your account and will be making the payment. It’s a fundamental part of identifying where the money is coming from.

Your account details

Your full account number is printed on the cheque, usually near the bottom. This number is unique to your bank account and is how the bank identifies your specific funds. Your name and address might also be printed on the cheque, confirming you’re the account holder.

The cheque number

Every cheque in your cheque book has a unique number, printed at the bottom left. This number is very important for tracking your payments and for your bank’s records. Always note down the cheque number when you make a payment, as it helps you keep track of your transactions.

The MICR code explained

The MICR code, which stands for Magnetic Ink Character Recognition, is a special 9-digit number printed at the bottom of your cheque. It’s written in a special ink that computers can read very quickly. This code helps banks process cheques much faster and more accurately, preventing delays and errors. It includes details about your bank, branch, and cheque number.

Quick Context: The MICR code is like a unique digital fingerprint for your cheque and your bank branch. It allows automated machines to read and process cheques quickly, making banking more efficient for everyone.

How to Fill in a Cheque Correctly

Filling out a cheque correctly is crucial for its validity and your financial safety. Even small mistakes can cause delays or, worse, lead to fraud. Always take your time and follow these steps carefully.

Writing the date

The date field is usually at the top right of the cheque. You must write the current date, as cheques are only valid for three months from this date. For example, if you write a cheque on 1st January, it will be valid until 31st March. Make sure the date is clear and correct.

Who are you paying?

This is the “Payee” section, usually starting with “Pay” or “Pay to the order of”. Here, you write the full name of the person or company you want to pay. Be very precise with the spelling, as even a tiny mistake could mean the cheque cannot be cashed. For instance, if you’re paying “Ms. Priya Sharma”, write her full name exactly.

The amount in numbers

There’s a small box, often next to the payee name, where you write the amount of money in numbers. For example, if you’re paying five thousand rupees, you’d write “5000.00”. Always start close to the left edge of the box and draw a line through any empty space after the amount to prevent anyone from adding extra numbers.

The amount in words

Below the numerical amount, there’s a line where you write the amount in words. This is a very important security feature, as the bank will always refer to the amount in words if there’s a difference between the numbers and words. For five thousand rupees, you’d write “Rupees Five Thousand Only”. Always end with “Only” to prevent anyone from adding more words.

Your important signature

Your signature is your authorisation for the bank to make the payment. You must sign the cheque exactly as you’ve registered your signature with the bank. If your signature doesn’t match, the bank might refuse to process the cheque. Never pre-sign blank cheques, as this is extremely risky.

Avoiding empty spaces

This is a critical safety rule. After writing the payee’s name, the amount in numbers, and the amount in words, always draw a straight line through any remaining empty space. This stops fraudsters from adding extra names or increasing the amount, protecting your money.

Imagine Rina from Delhi wanted to pay her landlord, Mr. Sharma, ₹15,000 for rent. She carefully wrote “Mr. Sharma” for the payee and “15000.00” in the numbers box. However, she forgot to draw a line after the amount. A dishonest person could potentially add a “0” to make it “150000.00” and then try to alter the words too. By simply drawing a line, Rina could have prevented this risk.

Keeping Your Cheque Safe and Secure

Cheques are like cash, and you should treat them with the same level of care. There are specific ways to make your cheques even more secure, protecting you from potential fraud.

What is a crossed cheque?

A crossed cheque has two parallel lines drawn across the top left corner. This simple act makes the cheque much safer. When a cheque is crossed, the money cannot be paid out as cash over the counter. Instead, it must be deposited directly into a bank account. This means if the cheque falls into the wrong hands, the person can’t simply walk into a bank and get cash for it.

“Account Payee Only” cheques

Adding the words “Account Payee Only” between the two parallel lines of a crossed cheque provides an extra layer of security. This instruction tells the bank that the money can only be credited to the bank account of the person or company whose name is written as the payee. It prevents the cheque from being endorsed (signed over) to someone else, ensuring the funds reach the intended recipient directly.

Not leaving gaps

We’ve mentioned this before, but it’s worth repeating: always ensure you don’t leave any blank spaces when filling out a cheque. This applies to every field – the payee’s name, the amount in numbers, and the amount in words. Any gap is an invitation for someone to alter the cheque.

Storing your cheque book

Your cheque book should be stored as carefully as you would store cash or important documents. Keep it in a secure place, away from prying eyes and potential theft. Never leave it lying around openly. If your cheque book is lost or stolen, report it to your bank immediately so they can block any misuse.

Pro Tip: When you receive a new cheque book, count the number of cheques to ensure none are missing. Also, sign your name on the first page of the cheque book as a security measure.

What Happens If You Make a Mistake?

Mistakes happen, but when it comes to cheques, it’s important to know how to handle them correctly. Depending on the type of error, there are different steps you should take.

Correcting small errors

For very minor errors, like a small spelling mistake in the payee’s name, you might be able to correct it. You’d make the correction, cross out the old entry, write the correct one, and then sign your full signature next to the correction. However, banks are very strict about corrections, especially with the amount. It’s generally safer to issue a new cheque if the mistake is significant, particularly with the numbers or words.

Cancelling a cheque

If you’ve made a significant error, or if you decide you no longer want to use a particular cheque, you should cancel it. To do this, simply write “CANCELLED” in large letters across the face of the cheque. This clearly indicates that the cheque is no longer valid and prevents anyone from using it. Always keep cancelled cheques for your records, never tear them up and discard them.

Stopping a cheque payment

Sometimes, after issuing a cheque, you might realise you need to stop the payment. Perhaps you’ve changed your mind, or there’s a dispute with the payee. In such cases, you can request your bank to “stop payment” on that specific cheque. You’ll need the cheque number, the amount, and the payee’s name. It’s crucial to act quickly, as the bank can only stop payment if the cheque hasn’t been processed yet. Banks usually charge a fee for this service.

Suresh from Mumbai had issued a cheque to a vendor for a service. A day later, he realised the service wasn’t delivered as promised, and he wanted to stop the payment. He immediately called his bank’s customer service, provided the cheque number and details, and requested a stop payment. Because he acted quickly, the bank was able to stop the cheque before it was cleared, saving him potential trouble.

When Should You Not Use a Cheque?

While cheques are useful, they aren’t always the best or fastest option. Understanding their limitations helps you choose the right payment method for each situation.

Other ways to pay

In our modern world, many digital payment methods offer instant transfers and greater convenience. Services like online banking (using NEFT, RTGS, or IMPS) allow you to send money directly from your bank account to another, often within minutes. These digital options are usually faster, more trackable, and don’t require physical paper. For smaller, everyday transactions, digital payments are often preferred.

| Feature | Cheques | Digital Payments (e.g., NEFT/IMPS) |

| Speed | Can take 2-3 business days to clear | Often instant or within minutes |

| Physicality | Requires a physical paper document | Entirely digital, no paper needed |

| Tracking | Cheque stub, bank statement | Digital transaction ID, instant notifications |

| Convenience | Requires filling out, signing, and delivering | Can be done anytime, anywhere with internet access |

| Security Risk | Risk of fraud if lost or incorrectly filled | Risk of cyber fraud if details are compromised |

| Proof of Payment | Cheque image on statement | Digital transaction record |

Cheque processing times

Unlike instant digital transfers, cheques take time to clear. Once you deposit a cheque, your bank needs to send it to the drawer’s bank for verification and funds transfer. This process, known as the “clearing cycle,” can take 2-3 business days, or even longer if there’s a bank holiday or if the banks are in different cities. If you need to make an urgent payment, a cheque might not be the best choice.

Expired cheques

Cheques are not valid forever. In India, a cheque is typically valid for three months from the date it’s written. If someone tries to deposit a cheque after this period, the bank will reject it, marking it as “stale” or “out of date.” Always make sure to deposit cheques you receive promptly and ensure any cheques you issue will be presented within their validity period.

Common Confusion: Many people think a cheque is valid for six months. However, the Reserve Bank of India (RBI) reduced the validity period to three months from 1st April 2012. Always remember the three-month rule!

Important Things to Remember About Cheques

Using cheques safely and effectively comes down to a few key principles. By keeping these in mind, you can protect yourself and ensure smooth financial transactions.

Always be careful

Treat every cheque as if it were cash. A blank cheque with your signature is essentially a blank authorisation for someone to withdraw money from your account. Never be careless with your cheque book or individual cheques. Always double-check who you are giving a cheque to and why.

Double-check everything

Before you sign a cheque, take a moment to review every detail. Is the date correct? Is the payee’s name spelled accurately? Do the numerical and written amounts match exactly? Have you drawn lines through all empty spaces? A quick review can prevent significant problems later on.

Keep records of cheques

It’s vital to keep a record of every cheque you issue and receive. Most cheque books have a stub or counterfoil where you can note down the cheque number, date, payee, and amount. This record helps you reconcile your bank statements and serves as proof of payment. In today’s digital age, your bank’s mobile app or online banking portal also keeps a digital record of all your cheque transactions, which you should regularly check.

“Diligence in handling financial instruments like cheques is not just about following rules; it’s about safeguarding your hard-earned money and ensuring peace of mind.”

Mastering the cheque might seem like a lot of information, but it’s all about being careful and understanding the basics. By following these essential rules, you can confidently use cheques as a secure and reliable way to manage your payments, ensuring your money is always safe and goes exactly where you intend it to.

Conclusion

Understanding Mastering the Cheque: Essential Rules for Filling and Writing Safely can help you make informed decisions. By following the guidelines outlined above, you can navigate this topic confidently.