Understanding where your money comes from and where it goes is an essential aspect of being smart with your finances. It helps you plan for the future, make good decisions, and feel secure about your money. When it comes to keeping track of your bank account, there are two main ways to do this: using a traditional bank passbook or opting for a modern e-statement. Both offer effective methods to monitor your money, but they work differently. Let’s explore each one to help you decide which might be the best fit for your needs.

Why Keeping Track of Your Money Matters

What are financial records and why are they important for you?

Financial records are a history of all the money that moves in and out of your bank account. Think of them as a diary for your money, showing every deposit you make, every payment you send, and any interest you might earn. These records are extremely important because they give you a clear picture of your financial situation. By looking at them, you can understand your spending habits, see if you’re saving enough, and even spot any mistakes or unexpected transactions. Having these details at hand helps you manage your money wisely, ensuring you have enough for everyday needs and for those special things you might be saving up for.

How to Follow Your Money’s Journey.

Following your money’s journey means knowing exactly what happens to it after it enters your account. Did you buy something online? Did you withdraw cash? Did you pay a bill? Your financial records answer these questions. They allow you to see the flow of your money, which is essential for budgeting and making sure you stay on track with your financial goals. It gives you a sense of control and peace of mind, knowing that you are fully aware of your financial activities.

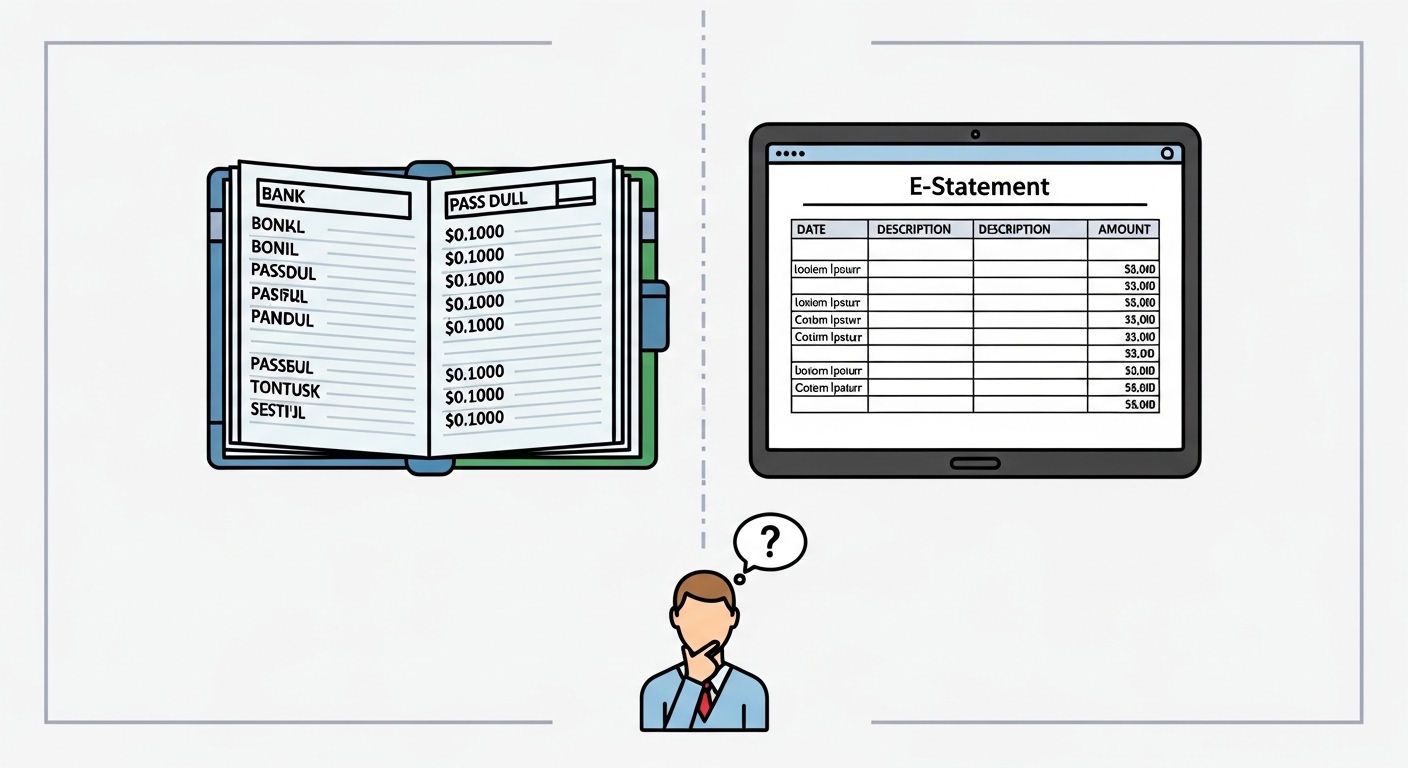

Getting to Know Your Bank Passbook

What is a bank passbook?

A bank passbook is a small, physical booklet that banks provide to their customers. It acts as a printed record of your bank account transactions. Whenever you deposit money, withdraw money, or receive interest, these details are printed directly into your passbook by the bank. It’s a traditional way of keeping up-to-date with your account, and many people still find it a reliable and comforting way to track their savings.

How does a passbook help you keep tabs on your savings?

Using a passbook gives you a tangible, physical record of your savings. You can hold it in your hand and clearly see all your transactions listed one after another, along with your current balance. For many, this physical presence makes it easier to understand their account activity. It’s particularly useful for basic savings accounts and helps you quickly check your balance or review recent transactions without needing any technology. It’s a straightforward way to keep an eye on your money, helping you budget and reconcile your account.

Are there any challenges when using a passbook?

While passbooks are beneficial, they do come with some challenges. The main one is that you typically need to visit your bank branch to get it updated. This means updates for your most recent transactions are not instantaneous. If you lose your passbook or if it gets damaged, it can be inconvenient to get a new one and transfer all your old records. Also, for accounts with many transactions, a passbook can fill up quickly, requiring a new one.

Discovering e-Statements

What is an e-Statement, and how does it work?

An e-statement, short for electronic statement, is a digital version of your bank statement. Instead of receiving a paper copy in the post, your bank sends it to you electronically, usually as a PDF file, via email or makes it available through your online banking portal or mobile banking application. It contains all the important information as a paper statement, including your deposits, withdrawals, and balance. It’s a modern, convenient way to receive and review your account activity.

How do e-Statements make managing your money simpler?

E-statements offer significant convenience. You can access them anytime, anywhere, as long as you have an internet connection and a device like a computer or smartphone. This means you can check your financial records even when you’re away from home. They are also environmentally friendly because they reduce the use of paper. Many people find it easier to store e-statements digitally, and you can often search through them quickly to find specific transactions. Plus, they are usually available more frequently than passbook updates, often monthly, giving you a regular overview of your finances.

What should you keep in mind when using e-Statements?

While e-statements are highly convenient, there are some key considerations. You’ll need reliable internet access and a device to view them. It’s crucial to keep your online banking passwords strong and unique, and always use secure internet connections to protect your information. You should also regularly check your email or online banking for new statements. It is important to exercise caution with suspicious emails pretending to be from your bank, as these could be attempts to trick you into revealing your personal details. Your bank will not request your full password or personal identification number (PIN) via email.

Comparing Your Options: Passbook vs. e-Statement

How you can check your money: physical book or digital screen?

The most obvious difference is how you interact with your records. With a passbook, you hold a physical book and read printed entries. To get updates, you need to visit a bank branch. With an e-statement, you view your records on a digital screen, like a computer, tablet, or phone. You can usually access these statements instantly, whenever you need them, without leaving your home.

Keeping your financial details safe and sound.

Both options require careful handling of your financial details. A passbook needs to be kept in a safe place at home, just like any other important document, to prevent it from being lost or stolen. For e-statements, security means protecting your digital access. This involves using strong passwords, being careful about where you access your online banking, and ensuring your devices are secure. Both methods are safe if you take responsible steps to protect your information.

How Frequently Can You View Account Updates?

With a passbook, updates are typically made when you visit your bank branch. This means you might not always have the latest transaction details immediately. E-statements, on the other hand, are usually generated monthly, but most online banking platforms allow you to view your transactions in near real-time, giving you a much more up-to-date look at your account activity.

Thinking about our planet: paper or paperless?

If you’re thinking about the environment, e-statements are the more eco-friendly choice. They are completely paperless, which helps reduce waste and saves trees. Passbooks, being physical books, do use paper, which contributes to paper consumption. Choosing e-statements is a small but positive step towards being more mindful of our planet.

When might one record be more useful than the other?

A passbook might be more useful if you prefer having a physical record, have limited access to the internet, or simply feel more comfortable with traditional banking methods. It’s also often preferred by those who make infrequent transactions. E-statements are generally more useful for people who are comfortable with technology, need frequent access to their account details, travel often, or want to keep digital records for easy searching and analysis.

Choosing What’s Right for You

Considering your own needs and how you like to manage your finances.

Ultimately, the choice between a bank passbook and an e-statement comes down to your personal preferences and how you like to manage your money. Think about what makes you feel most organised and secure. Do you prefer the tangible feel of a book, or the convenience of digital access? Consider your daily routine, your comfort with technology, and how often you need to check your account. There’s no single right answer; it’s about what works best for you and your lifestyle.

Smart tips for safeguarding your money records.

No matter which option you choose, it’s always prudent to safeguard your money records carefully. Review your statements or passbook entries regularly to ensure accuracy. If you use a passbook, keep it in a safe place. If you use e-statements, ensure they are saved securely on your computer or in a cloud storage service, and always use strong passwords for your online banking. If you ever spot something unusual or incorrect, contact your bank immediately to resolve it. Developing a consistent habit of checking your finances is key to good money management.

Final Thoughts on Tracking Your Finances

Both options are valuable; it depends on what suits you best.

Both bank passbooks and e-statements are effective tools for tracking your finances. They both serve the same fundamental purpose: to give you a clear record of your money’s movements. The “best” option isn’t universal; it truly depends on your individual needs, preferences, and how you prefer to interact with your financial information. Some people appreciate the traditional feel of a passbook, while others embrace the digital convenience of e-statements.

The lasting importance of knowing where your money goes.

Regardless of whether you choose a passbook or an e-statement, the most important thing is to consistently know where your money goes. Staying informed about your financial transactions helps you make better decisions, plan for your future, and work towards your financial goals. It empowers you with knowledge and gives you confidence in managing your money effectively. Regularly reviewing your financial records is a habit that will serve you well throughout your life.